3.10 Financial liabilities

The LGU’s financial liabilities include payables and borrowings which the

Municipality is committed to pay for goods or services received. These also include

amounts entrusted to/withheld by outside sources/offices and personnel for which the

Municipality is acting as a trustee or administrator.

Payables are recognized and recorded in the book of accounts only upon acceptance

of goods and rendering of service to the Municipality.

Loans contracted by the Municipality are recognized upon receipt of the proceeds

from creditors. Interest payable is normally settled quarterly throughout the financial

year.

3.11 Equity

Equity represents the difference between the assets and liabilities. The amount

available for operations is computed by deducting the following from the ending

balance of Government Equity:

a. Equity set aside to finance capital projects with appropriations provided in

previous years (continuing appropriations)

b. Portion pertaining to receivables, inventories, prepayments and other current

assets

c. Portion pertaining to property, plant and equipment including public infrastructure

in process

d. Amount reserved for Local Disaster Risk Reduction and Management Fund

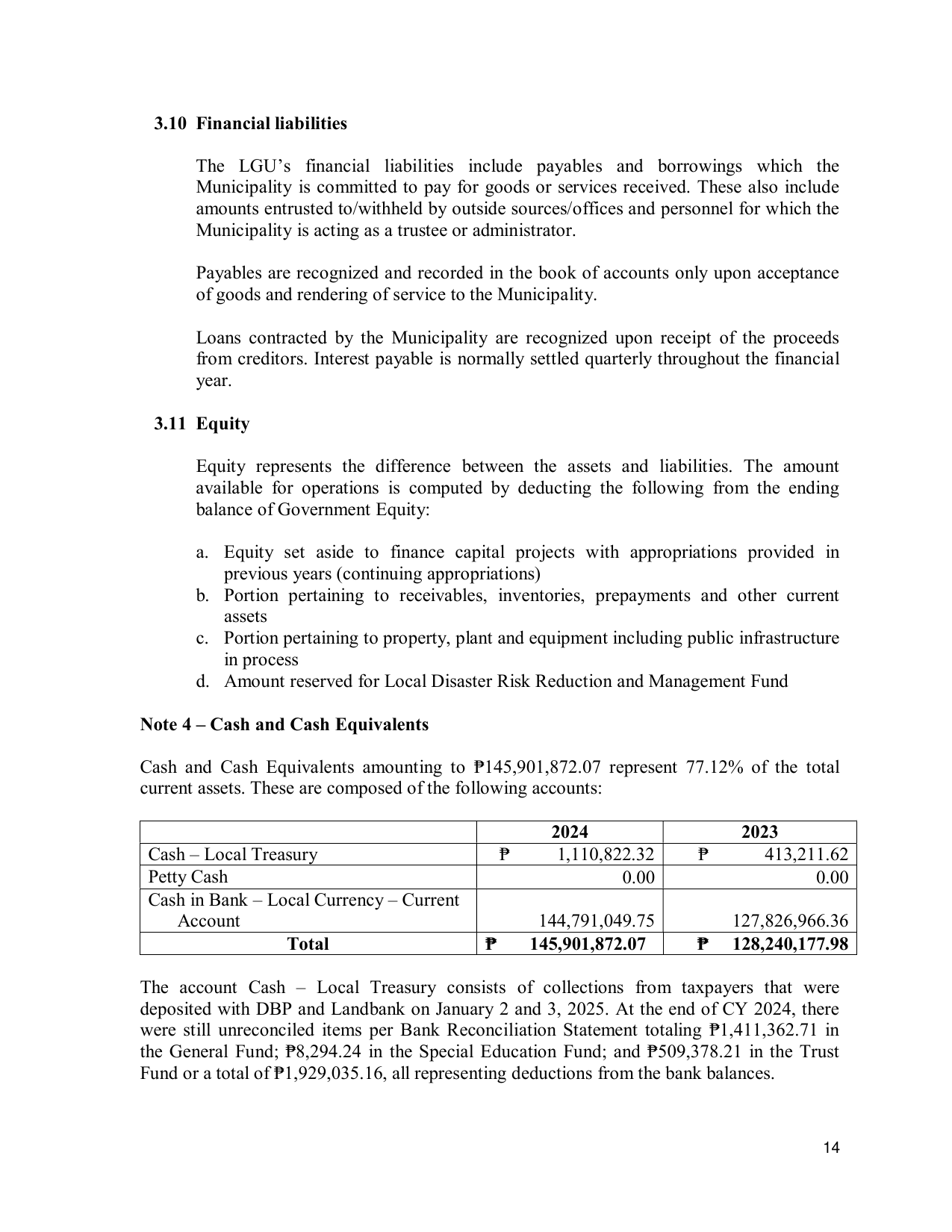

Note 4 – Cash and Cash Equivalents

Cash and Cash Equivalents amounting to ₱145,901,872.07 represent 77.12% of the total

current assets. These are composed of the following accounts:

2024 2023

Cash – Local Treasury ₱ 1,110,822.32 ₱ 413,211.62

Petty Cash 0.00 0.00

Cash in Bank – Local Currency – Current

Account 144,791,049.75 127,826,966.36

Total ₱ 145,901,872.07 ₱ 128,240,177.98

The account Cash – Local Treasury consists of collections from taxpayers that were

deposited with DBP and Landbank on January 2 and 3, 2025. At the end of CY 2024, there

were still unreconciled items per Bank Reconciliation Statement totaling ₱1,411,362.71 in

the General Fund; ₱8,294.24 in the Special Education Fund; and ₱509,378.21 in the Trust

Fund or a total of ₱1,929,035.16, all representing deductions from the bank balances.

14