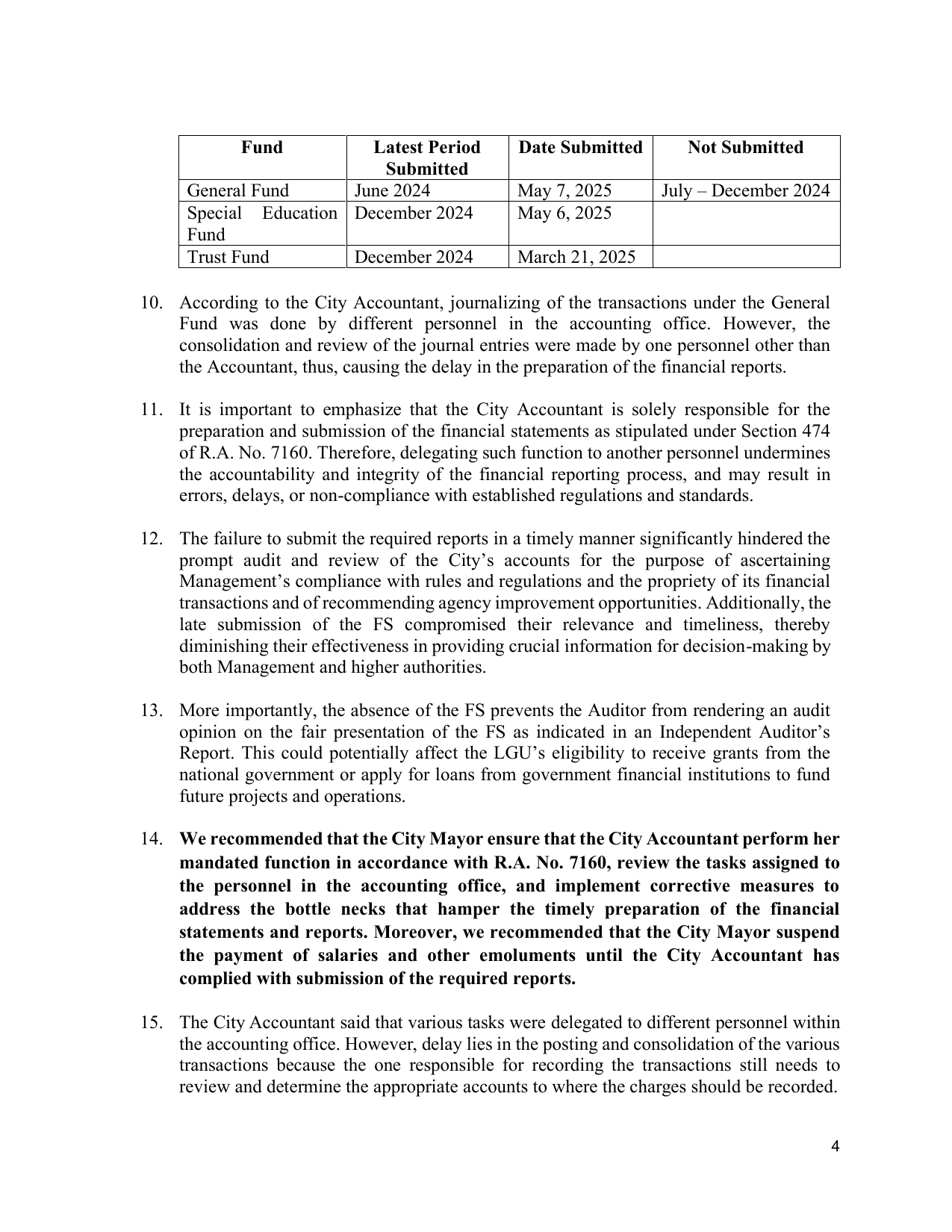

Fund Latest Period Date Submitted Not Submitted

Submitted

General Fund June 2024 May 7, 2025 July – December 2024

Special Education December 2024 May 6, 2025

Fund

Trust Fund December 2024 March 21, 2025

10. According to the City Accountant, journalizing of the transactions under the General

Fund was done by different personnel in the accounting office. However, the

consolidation and review of the journal entries were made by one personnel other than

the Accountant, thus, causing the delay in the preparation of the financial reports.

11. It is important to emphasize that the City Accountant is solely responsible for the

preparation and submission of the financial statements as stipulated under Section 474

of R.A. No. 7160. Therefore, delegating such function to another personnel undermines

the accountability and integrity of the financial reporting process, and may result in

errors, delays, or non-compliance with established regulations and standards.

12. The failure to submit the required reports in a timely manner significantly hindered the

prompt audit and review of the City’s accounts for the purpose of ascertaining

Management’s compliance with rules and regulations and the propriety of its financial

transactions and of recommending agency improvement opportunities. Additionally, the

late submission of the FS compromised their relevance and timeliness, thereby

diminishing their effectiveness in providing crucial information for decision-making by

both Management and higher authorities.

13. More importantly, the absence of the FS prevents the Auditor from rendering an audit

opinion on the fair presentation of the FS as indicated in an Independent Auditor’s

Report. This could potentially affect the LGU’s eligibility to receive grants from the

national government or apply for loans from government financial institutions to fund

future projects and operations.

14. We recommended that the City Mayor ensure that the City Accountant perform her

mandated function in accordance with R.A. No. 7160, review the tasks assigned to

the personnel in the accounting office, and implement corrective measures to

address the bottle necks that hamper the timely preparation of the financial

statements and reports. Moreover, we recommended that the City Mayor suspend

the payment of salaries and other emoluments until the City Accountant has

complied with submission of the required reports.

15. The City Accountant said that various tasks were delegated to different personnel within

the accounting office. However, delay lies in the posting and consolidation of the various

transactions because the one responsible for recording the transactions still needs to

review and determine the appropriate accounts to where the charges should be recorded.

4