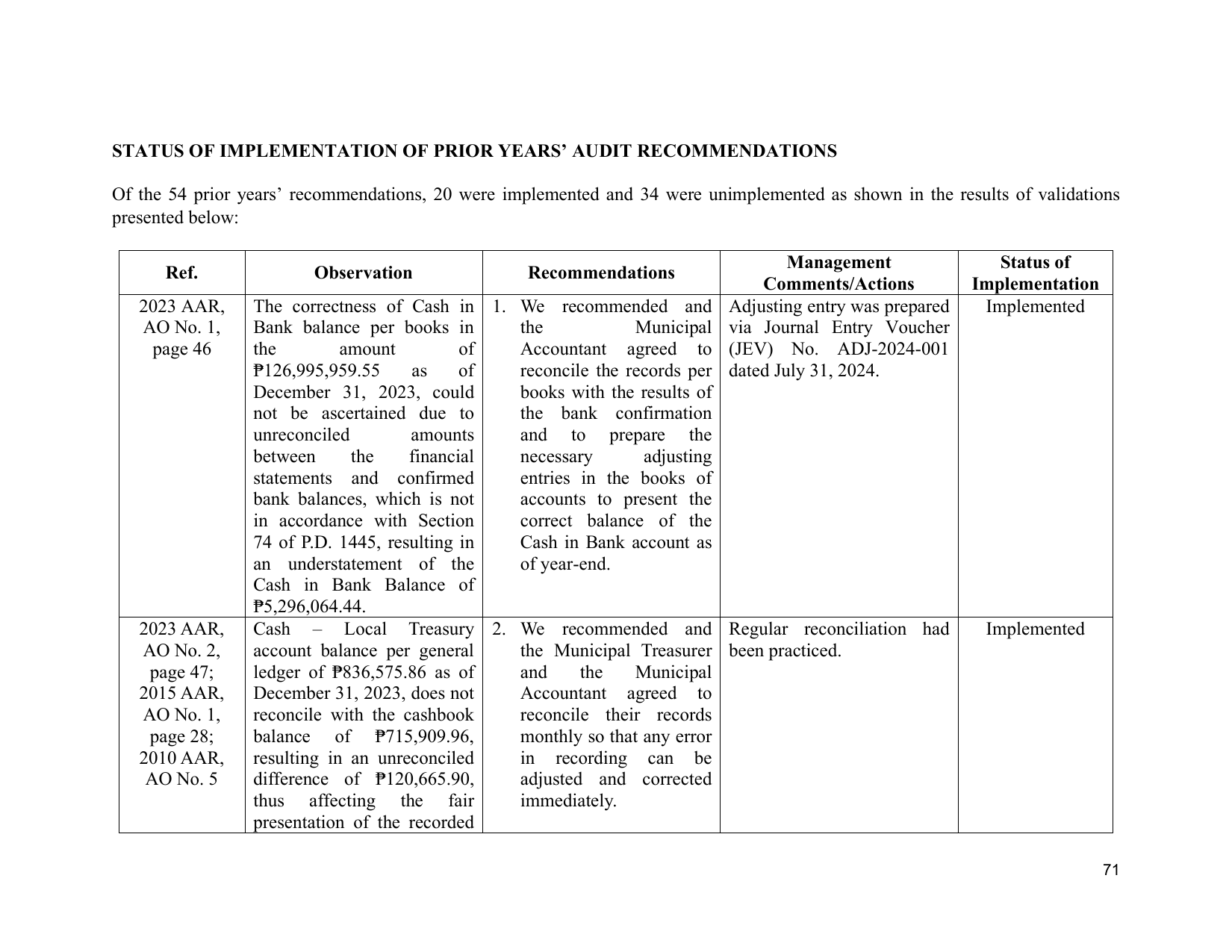

STATUS OF IMPLEMENTATION OF PRIOR YEARS’ AUDIT RECOMMENDATIONS

Of the 54 prior years’ recommendations, 20 were implemented and 34 were unimplemented as shown in the results of validations

presented below:

Management Status of

Ref. Observation Recommendations

Comments/Actions Implementation

2023 AAR, The correctness of Cash in 1. We recommended and Adjusting entry was prepared Implemented

AO No. 1, Bank balance per books in the Municipal via Journal Entry Voucher

page 46 the amount of Accountant agreed to (JEV) No. ADJ-2024-001

₱126,995,959.55 as of reconcile the records per dated July 31, 2024.

December 31, 2023, could books with the results of

not be ascertained due to the bank confirmation

unreconciled amounts and to prepare the

between the financial necessary adjusting

statements and confirmed entries in the books of

bank balances, which is not accounts to present the

in accordance with Section correct balance of the

74 of P.D. 1445, resulting in Cash in Bank account as

an understatement of the of year-end.

Cash in Bank Balance of

₱5,296,064.44.

2023 AAR, Cash – Local Treasury 2. We recommended and Regular reconciliation had Implemented

AO No. 2, account balance per general the Municipal Treasurer been practiced.

page 47; ledger of ₱836,575.86 as of and the Municipal

2015 AAR, December 31, 2023, does not Accountant agreed to

AO No. 1, reconcile with the cashbook reconcile their records

page 28; balance of ₱715,909.96, monthly so that any error

2010 AAR, resulting in an unreconciled in recording can be

AO No. 5 difference of ₱120,665.90, adjusted and corrected

thus affecting the fair immediately.

presentation of the recorded

71