6.11.2. The Municipal Treasurer to furnish the Municipal Accountant a duly

certified list of taxpayers with the amount due and collectible for the

current year as basis for recording the RPT Receivable and SET

Receivable accounts in compliance with Section 20 of the NGAS

Manual for LGUs, Volume I.

6.12. During the exit conference, the Municipal Accountant explained that on the first

year that he recognized RPT/SET Receivables, he did not recognize the whole

amount because it would overstate the assets since he deemed that most of that

figure would not actually be collected. With the advice of the then Audit Team

Leader, he just disclosed the discrepancy in the Notes to the Financial Statements

(FS) and only recorded the current year portion expected to be collected by the

Office of the Municipal Treasurer.

6.13. Additionally, the Municipal Treasurer disclosed that the Office of the Municipal

Assessor was undertaking cleansing of its records to determine the final value of

RPT/SET Receivables.

6.14. The Audit Team likewise instructed the Municipal Accountant to disclose the

discrepancy in the Notes to the FS.

Deposit of Collections

7. The Municipal Treasurer did not deposit intact his collections of ₱339,550.22 to the

authorized depository bank at the end of the year, contrary to Section 69 of

Presidential Decree (P.D.) No. 1445 thereby exposing government funds to the risk

of misappropriation and possible loss.

7.1. Section 69 P.D. 1445 or the State Audit Code of the Philippines on deposit of

moneys in the treasury provides that:

“(1) Public officers authorized to receive and collect moneys arising from

taxes, revenues, or receipts of any kind shall remit or deposit intact the

full amounts so received and collected by them to the treasury of the

agency concerned and credited to the particular accounts to which the

said moneys belong.”

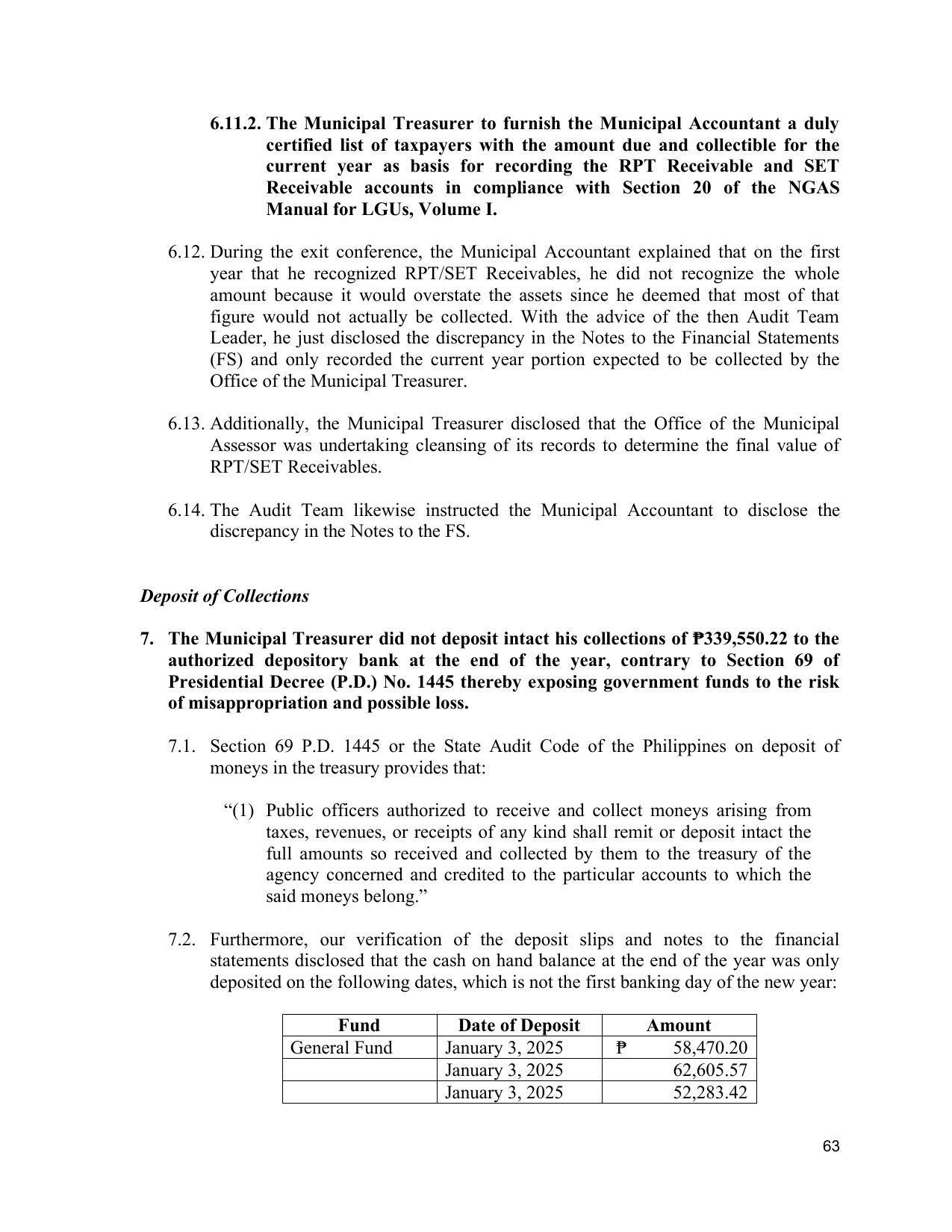

7.2. Furthermore, our verification of the deposit slips and notes to the financial

statements disclosed that the cash on hand balance at the end of the year was only

deposited on the following dates, which is not the first banking day of the new year:

Fund Date of Deposit Amount

General Fund January 3, 2025 ₱ 58,470.20

January 3, 2025 62,605.57

January 3, 2025 52,283.42

63