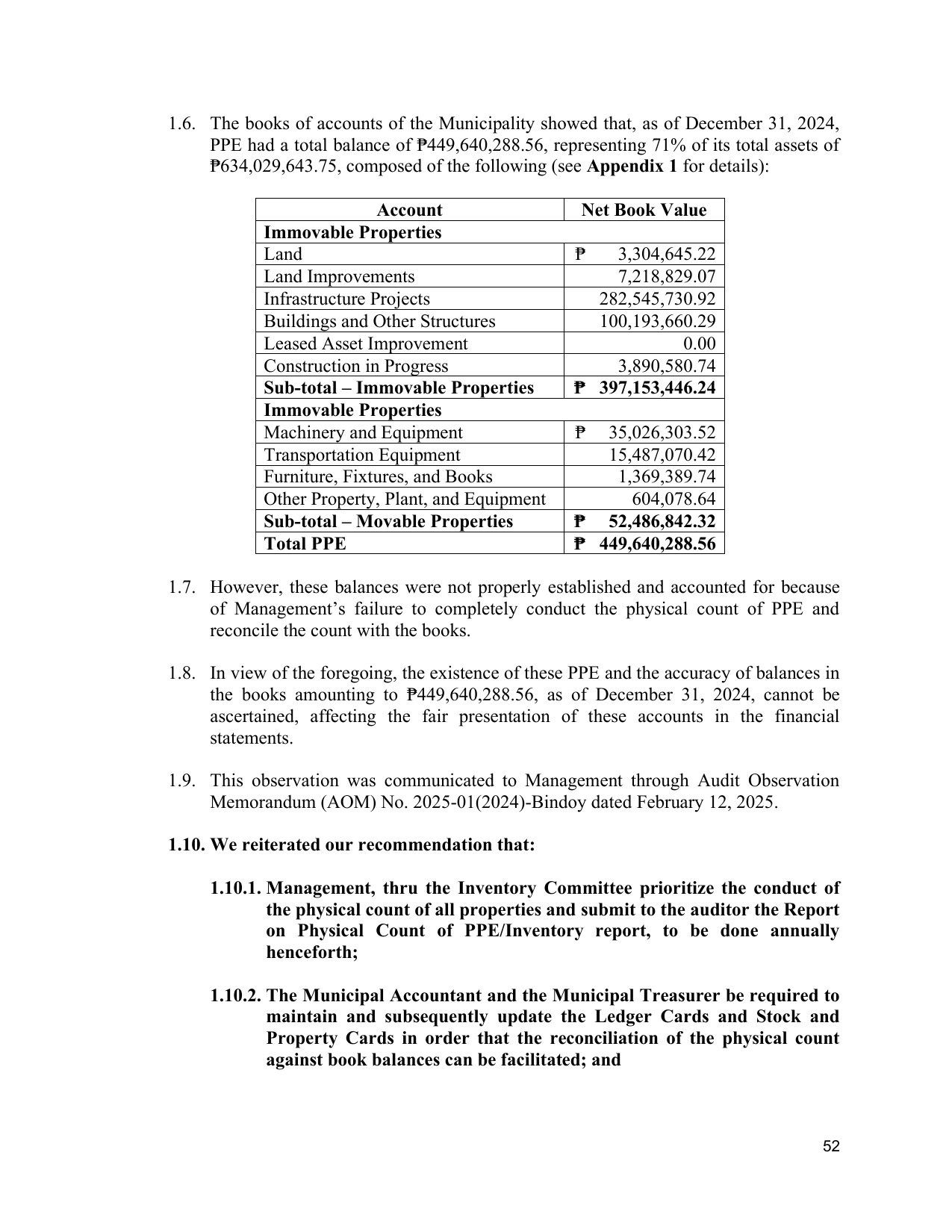

1.6. The books of accounts of the Municipality showed that, as of December 31, 2024,

PPE had a total balance of ₱449,640,288.56, representing 71% of its total assets of

₱634,029,643.75, composed of the following (see Appendix 1 for details):

Account Net Book Value

Immovable Properties

Land ₱ 3,304,645.22

Land Improvements 7,218,829.07

Infrastructure Projects 282,545,730.92

Buildings and Other Structures 100,193,660.29

Leased Asset Improvement 0.00

Construction in Progress 3,890,580.74

Sub-total – Immovable Properties ₱ 397,153,446.24

Immovable Properties

Machinery and Equipment ₱ 35,026,303.52

Transportation Equipment 15,487,070.42

Furniture, Fixtures, and Books 1,369,389.74

Other Property, Plant, and Equipment 604,078.64

Sub-total – Movable Properties ₱ 52,486,842.32

Total PPE ₱ 449,640,288.56

1.7. However, these balances were not properly established and accounted for because

of Management’s failure to completely conduct the physical count of PPE and

reconcile the count with the books.

1.8. In view of the foregoing, the existence of these PPE and the accuracy of balances in

the books amounting to ₱449,640,288.56, as of December 31, 2024, cannot be

ascertained, affecting the fair presentation of these accounts in the financial

statements.

1.9. This observation was communicated to Management through Audit Observation

Memorandum (AOM) No. 2025-01(2024)-Bindoy dated February 12, 2025.

1.10. We reiterated our recommendation that:

1.10.1. Management, thru the Inventory Committee prioritize the conduct of

the physical count of all properties and submit to the auditor the Report

on Physical Count of PPE/Inventory report, to be done annually

henceforth;

1.10.2. The Municipal Accountant and the Municipal Treasurer be required to

maintain and subsequently update the Ledger Cards and Stock and

Property Cards in order that the reconciliation of the physical count

against book balances can be facilitated; and

52