11.8 Management assured the audit team that they are committed in improving its

procurement process and ensuring compliance with the Government Procurement

Reform Act.

Granting of cash advances despite non-liquidation of previous cash advances

12. Cash advances for salaries, wages, allowances, honoraria, and other current

operating expenses were granted to disbursing officers despite not fully liquidating

previous cash advances for the same purpose, inconsistent with Section 4.1.2 of

COA Circular No. 97-002, resulting in overlapping cash advances and exposing

government funds to the risk of loss through misapplication.

12.1 Commission on Audit (COA) Circular No. 97-002 dated February 10, 1997,

provides the rules and regulations on the granting, utilization, and liquidation of

cash advances. Section 4.1.2 thereof explicitly states that no additional cash

advances shall be allowed to any official or employee unless the previous cash

advance given to him is first settled or a proper accounting thereof is made.

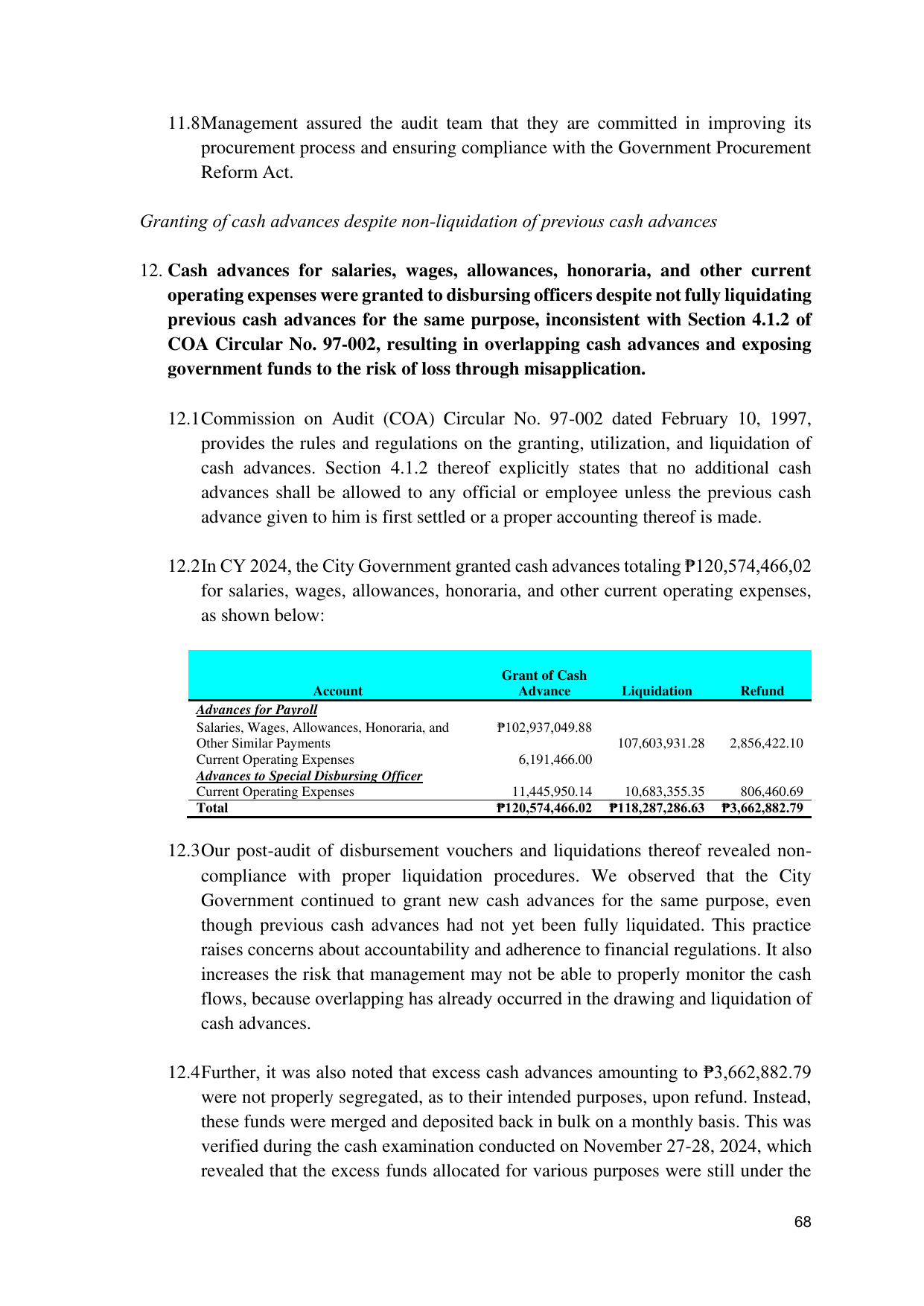

12.2 In CY 2024, the City Government granted cash advances totaling ₱120,574,466,02

for salaries, wages, allowances, honoraria, and other current operating expenses,

as shown below:

Grant of Cash

Account Advance Liquidation Refund

Advances for Payroll

Salaries, Wages, Allowances, Honoraria, and ₱102,937,049.88

Other Similar Payments 107,603,931.28 2,856,422.10

Current Operating Expenses 6,191,466.00

Advances to Special Disbursing Officer

Current Operating Expenses 11,445,950.14 10,683,355.35 806,460.69

Total ₱120,574,466.02 ₱118,287,286.63 ₱3,662,882.79

12.3 Our post-audit of disbursement vouchers and liquidations thereof revealed non-

compliance with proper liquidation procedures. We observed that the City

Government continued to grant new cash advances for the same purpose, even

though previous cash advances had not yet been fully liquidated. This practice

raises concerns about accountability and adherence to financial regulations. It also

increases the risk that management may not be able to properly monitor the cash

flows, because overlapping has already occurred in the drawing and liquidation of

cash advances.

12.4 Further, it was also noted that excess cash advances amounting to ₱3,662,882.79

were not properly segregated, as to their intended purposes, upon refund. Instead,

these funds were merged and deposited back in bulk on a monthly basis. This was

verified during the cash examination conducted on November 27-28, 2024, which

revealed that the excess funds allocated for various purposes were still under the

68