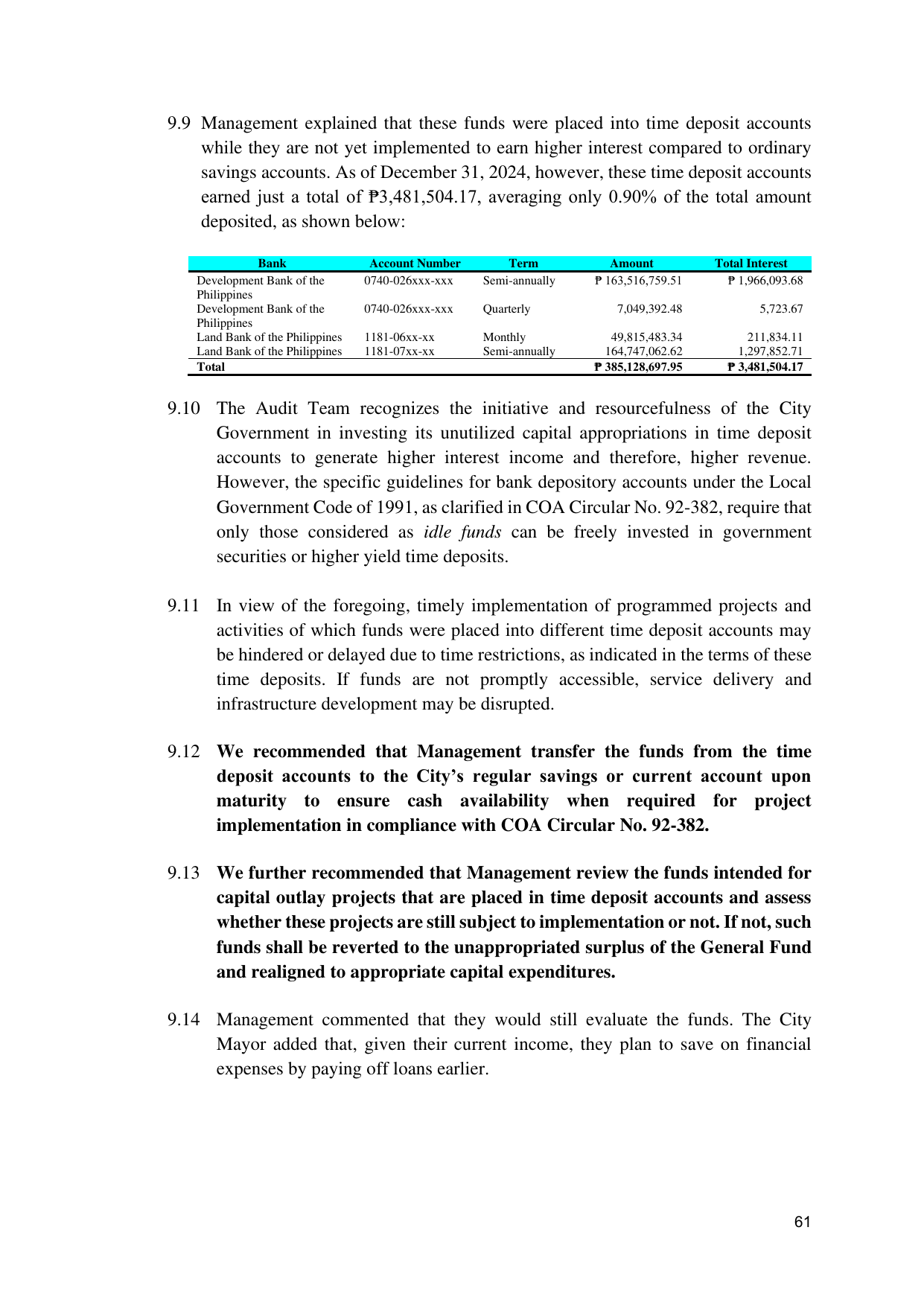

9.9 Management explained that these funds were placed into time deposit accounts

while they are not yet implemented to earn higher interest compared to ordinary

savings accounts. As of December 31, 2024, however, these time deposit accounts

earned just a total of ₱3,481,504.17, averaging only 0.90% of the total amount

deposited, as shown below:

Bank Account Number Term Amount Total Interest

Development Bank of the 0740-026xxx-xxx Semi-annually ₱ 163,516,759.51 ₱ 1,966,093.68

Philippines

Development Bank of the 0740-026xxx-xxx Quarterly 7,049,392.48 5,723.67

Philippines

Land Bank of the Philippines 1181-06xx-xx Monthly 49,815,483.34 211,834.11

Land Bank of the Philippines 1181-07xx-xx Semi-annually 164,747,062.62 1,297,852.71

Total ₱ 385,128,697.95 ₱ 3,481,504.17

9.10 The Audit Team recognizes the initiative and resourcefulness of the City

Government in investing its unutilized capital appropriations in time deposit

accounts to generate higher interest income and therefore, higher revenue.

However, the specific guidelines for bank depository accounts under the Local

Government Code of 1991, as clarified in COA Circular No. 92-382, require that

only those considered as idle funds can be freely invested in government

securities or higher yield time deposits.

9.11 In view of the foregoing, timely implementation of programmed projects and

activities of which funds were placed into different time deposit accounts may

be hindered or delayed due to time restrictions, as indicated in the terms of these

time deposits. If funds are not promptly accessible, service delivery and

infrastructure development may be disrupted.

9.12 We recommended that Management transfer the funds from the time

deposit accounts to the City’s regular savings or current account upon

maturity to ensure cash availability when required for project

implementation in compliance with COA Circular No. 92-382.

9.13 We further recommended that Management review the funds intended for

capital outlay projects that are placed in time deposit accounts and assess

whether these projects are still subject to implementation or not. If not, such

funds shall be reverted to the unappropriated surplus of the General Fund

and realigned to appropriate capital expenditures.

9.14 Management commented that they would still evaluate the funds. The City

Mayor added that, given their current income, they plan to save on financial

expenses by paying off loans earlier.

61