6.5 However, during our examination of the utilization of the 20 percent DF, which

included verifying the projects funded through the account and the corresponding

journal entries for each charge, we observed that the funds for the 20 percent DF

were deposited into the General Fund bank account of the City Government, rather

than a separate bank account designated for this specific purpose.

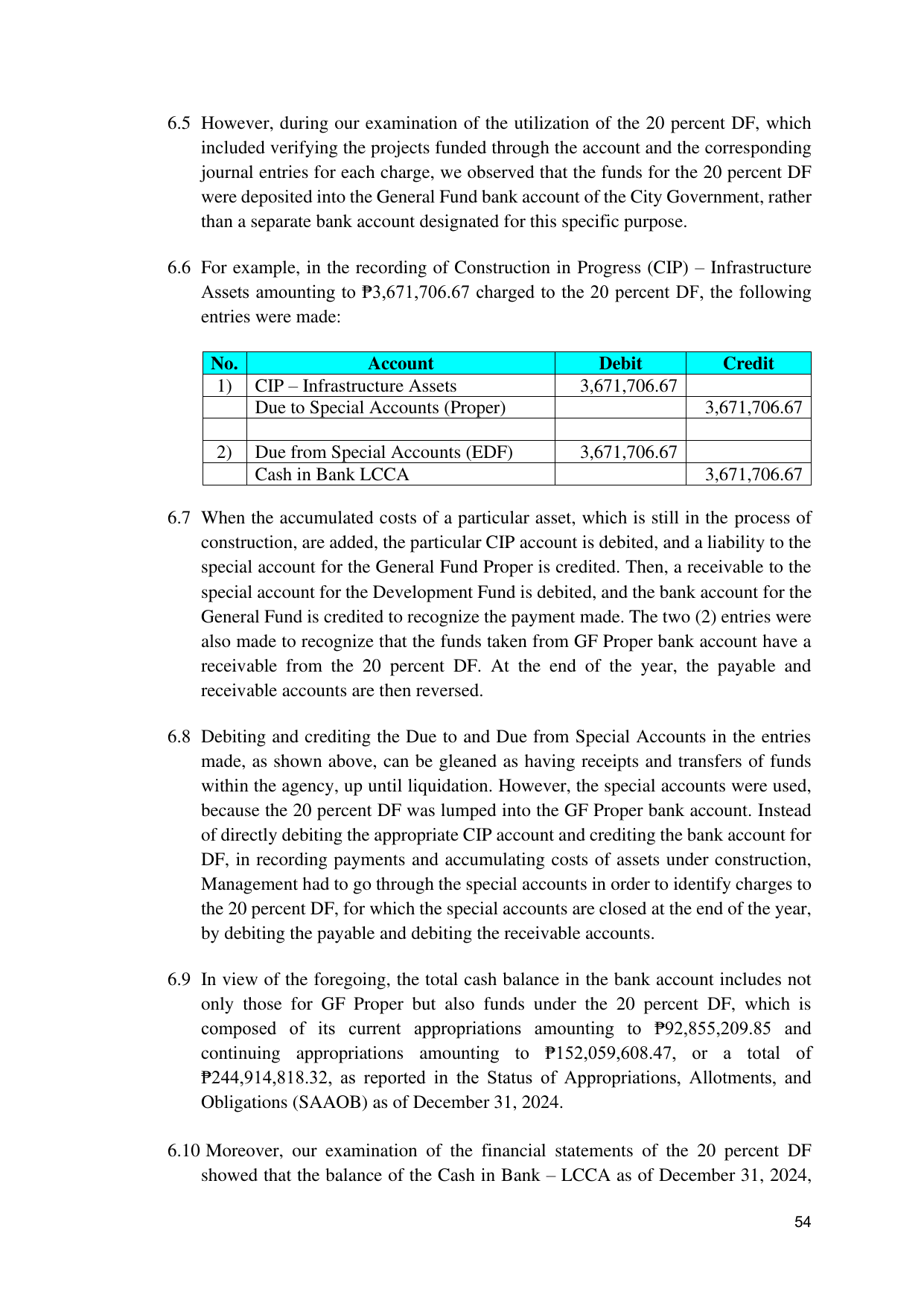

6.6 For example, in the recording of Construction in Progress (CIP) – Infrastructure

Assets amounting to ₱3,671,706.67 charged to the 20 percent DF, the following

entries were made:

No. Account Debit Credit

1) CIP – Infrastructure Assets 3,671,706.67

Due to Special Accounts (Proper) 3,671,706.67

2) Due from Special Accounts (EDF) 3,671,706.67

Cash in Bank LCCA 3,671,706.67

6.7 When the accumulated costs of a particular asset, which is still in the process of

construction, are added, the particular CIP account is debited, and a liability to the

special account for the General Fund Proper is credited. Then, a receivable to the

special account for the Development Fund is debited, and the bank account for the

General Fund is credited to recognize the payment made. The two (2) entries were

also made to recognize that the funds taken from GF Proper bank account have a

receivable from the 20 percent DF. At the end of the year, the payable and

receivable accounts are then reversed.

6.8 Debiting and crediting the Due to and Due from Special Accounts in the entries

made, as shown above, can be gleaned as having receipts and transfers of funds

within the agency, up until liquidation. However, the special accounts were used,

because the 20 percent DF was lumped into the GF Proper bank account. Instead

of directly debiting the appropriate CIP account and crediting the bank account for

DF, in recording payments and accumulating costs of assets under construction,

Management had to go through the special accounts in order to identify charges to

the 20 percent DF, for which the special accounts are closed at the end of the year,

by debiting the payable and debiting the receivable accounts.

6.9 In view of the foregoing, the total cash balance in the bank account includes not

only those for GF Proper but also funds under the 20 percent DF, which is

composed of its current appropriations amounting to ₱92,855,209.85 and

continuing appropriations amounting to ₱152,059,608.47, or a total of

₱244,914,818.32, as reported in the Status of Appropriations, Allotments, and

Obligations (SAAOB) as of December 31, 2024.

6.10 Moreover, our examination of the financial statements of the 20 percent DF

showed that the balance of the Cash in Bank – LCCA as of December 31, 2024,

54