of accounting, transactions and events are recorded in the accounting records and

recognized in the financial statements in the period to which they relate.

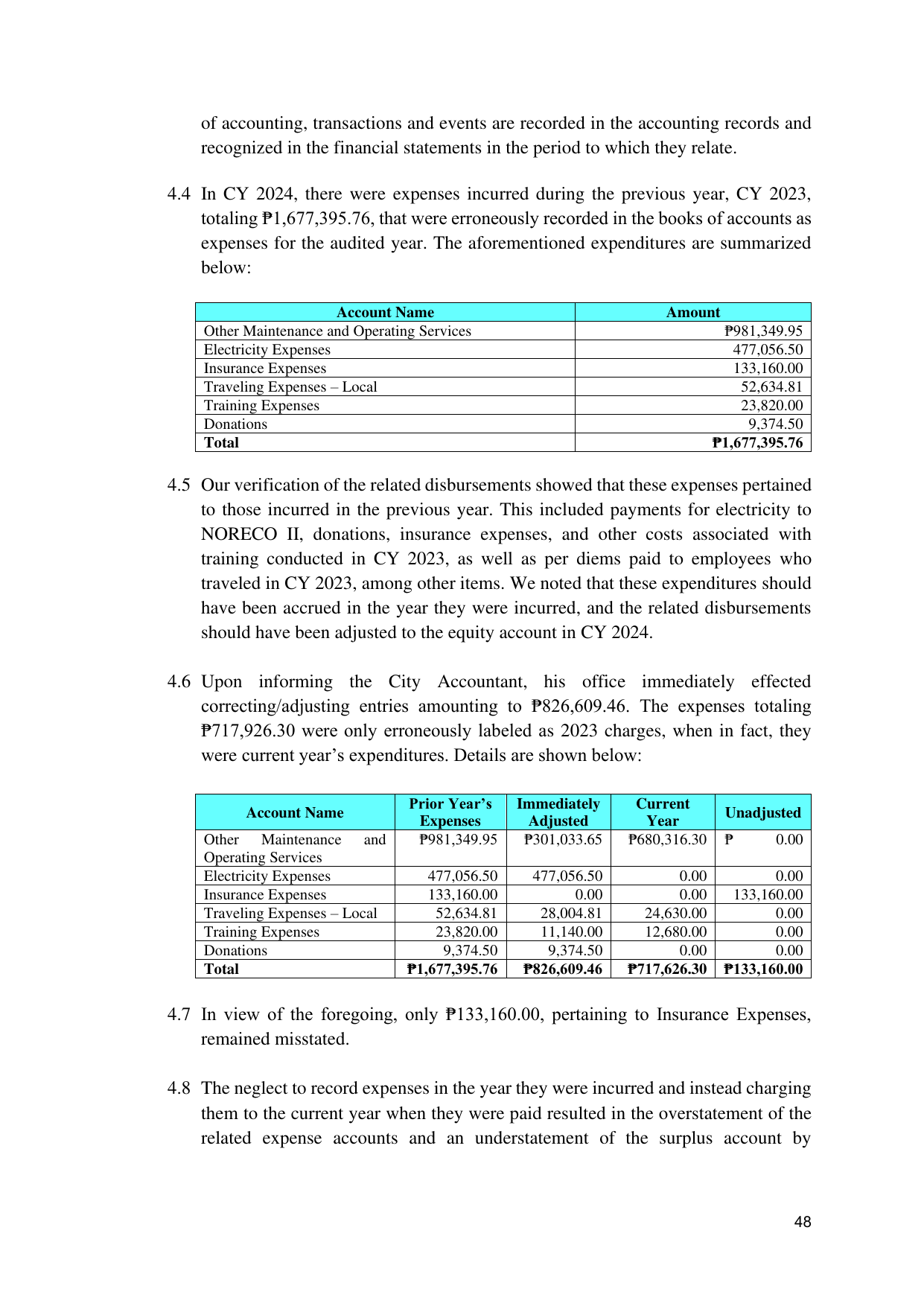

4.4 In CY 2024, there were expenses incurred during the previous year, CY 2023,

totaling ₱1,677,395.76, that were erroneously recorded in the books of accounts as

expenses for the audited year. The aforementioned expenditures are summarized

below:

Account Name Amount

Other Maintenance and Operating Services ₱981,349.95

Electricity Expenses 477,056.50

Insurance Expenses 133,160.00

Traveling Expenses – Local 52,634.81

Training Expenses 23,820.00

Donations 9,374.50

Total ₱1,677,395.76

4.5 Our verification of the related disbursements showed that these expenses pertained

to those incurred in the previous year. This included payments for electricity to

NORECO II, donations, insurance expenses, and other costs associated with

training conducted in CY 2023, as well as per diems paid to employees who

traveled in CY 2023, among other items. We noted that these expenditures should

have been accrued in the year they were incurred, and the related disbursements

should have been adjusted to the equity account in CY 2024.

4.6 Upon informing the City Accountant, his office immediately effected

correcting/adjusting entries amounting to ₱826,609.46. The expenses totaling

₱717,926.30 were only erroneously labeled as 2023 charges, when in fact, they

were current year’s expenditures. Details are shown below:

Prior Year’s Immediately Current

Account Name Unadjusted

Expenses Adjusted Year

Other Maintenance and ₱981,349.95 ₱301,033.65 ₱680,316.30 ₱ 0.00

Operating Services

Electricity Expenses 477,056.50 477,056.50 0.00 0.00

Insurance Expenses 133,160.00 0.00 0.00 133,160.00

Traveling Expenses – Local 52,634.81 28,004.81 24,630.00 0.00

Training Expenses 23,820.00 11,140.00 12,680.00 0.00

Donations 9,374.50 9,374.50 0.00 0.00

Total ₱1,677,395.76 ₱826,609.46 ₱717,626.30 ₱133,160.00

4.7 In view of the foregoing, only ₱133,160.00, pertaining to Insurance Expenses,

remained misstated.

4.8 The neglect to record expenses in the year they were incurred and instead charging

them to the current year when they were paid resulted in the overstatement of the

related expense accounts and an understatement of the surplus account by

48