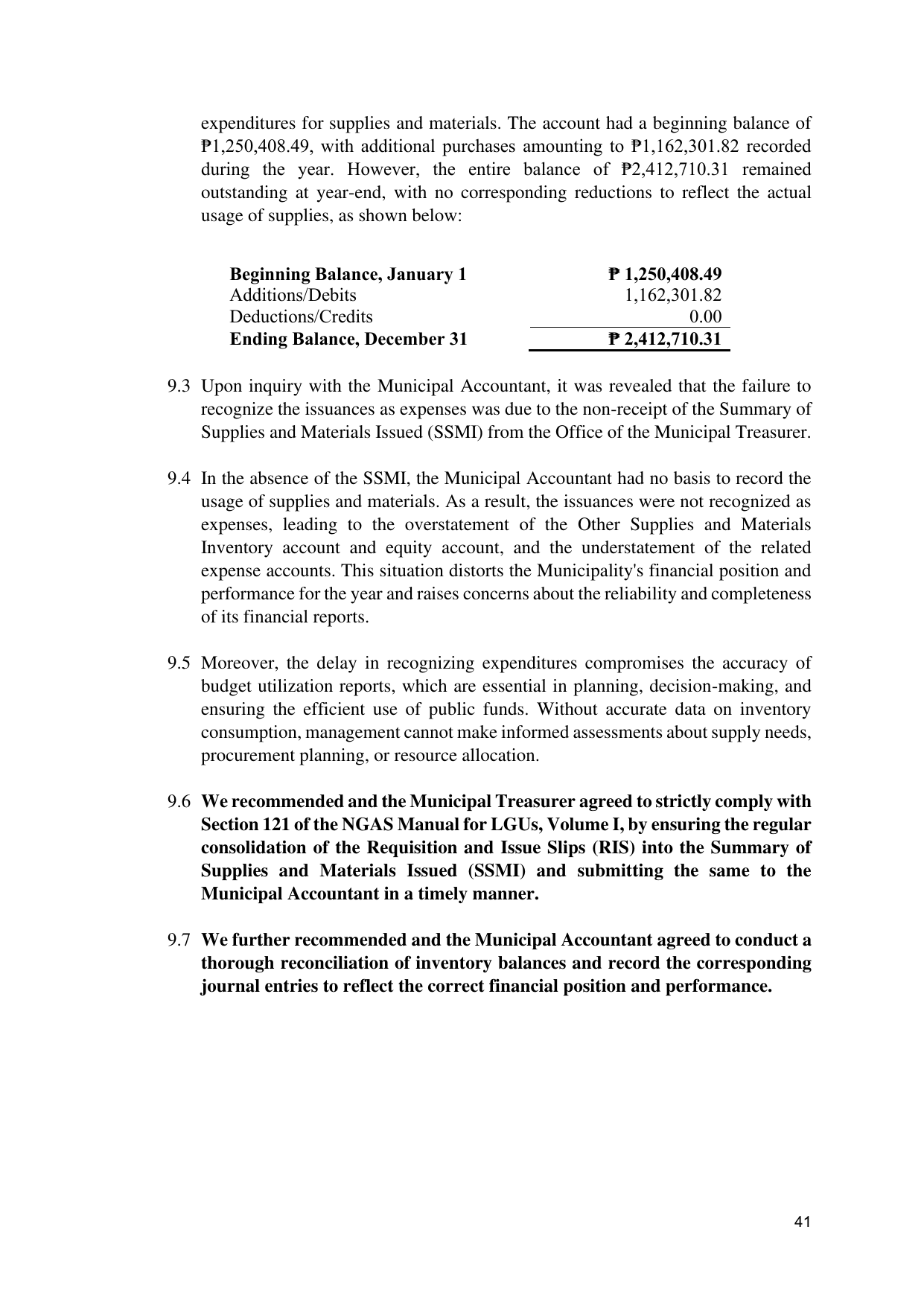

expenditures for supplies and materials. The account had a beginning balance of

₱1,250,408.49, with additional purchases amounting to ₱1,162,301.82 recorded

during the year. However, the entire balance of ₱2,412,710.31 remained

outstanding at year-end, with no corresponding reductions to reflect the actual

usage of supplies, as shown below:

Beginning Balance, January 1 ₱ 1,250,408.49

Additions/Debits 1,162,301.82

Deductions/Credits 0.00

Ending Balance, December 31 ₱ 2,412,710.31

9.3 Upon inquiry with the Municipal Accountant, it was revealed that the failure to

recognize the issuances as expenses was due to the non-receipt of the Summary of

Supplies and Materials Issued (SSMI) from the Office of the Municipal Treasurer.

9.4 In the absence of the SSMI, the Municipal Accountant had no basis to record the

usage of supplies and materials. As a result, the issuances were not recognized as

expenses, leading to the overstatement of the Other Supplies and Materials

Inventory account and equity account, and the understatement of the related

expense accounts. This situation distorts the Municipality's financial position and

performance for the year and raises concerns about the reliability and completeness

of its financial reports.

9.5 Moreover, the delay in recognizing expenditures compromises the accuracy of

budget utilization reports, which are essential in planning, decision-making, and

ensuring the efficient use of public funds. Without accurate data on inventory

consumption, management cannot make informed assessments about supply needs,

procurement planning, or resource allocation.

9.6 We recommended and the Municipal Treasurer agreed to strictly comply with

Section 121 of the NGAS Manual for LGUs, Volume I, by ensuring the regular

consolidation of the Requisition and Issue Slips (RIS) into the Summary of

Supplies and Materials Issued (SSMI) and submitting the same to the

Municipal Accountant in a timely manner.

9.7 We further recommended and the Municipal Accountant agreed to conduct a

thorough reconciliation of inventory balances and record the corresponding

journal entries to reflect the correct financial position and performance.

41