7.3 In the Municipality, the Treasurer receives the monthly BS from the bank, along

with the copies of DM/CM. Thus, it is crucial for the Municipal Treasurer to

coordinate with the Municipal Accountant to ensure that the latter receives copies

of the documents/reports from the bank. Additionally, it is essential for the

Municipal Accountant to request copies of these documents/reports from the

Office of the Municipal Treasurer on a monthly basis, as he/she is required to

prepare monthly BRS, which will be submitted to the assigned Auditor, to confirm

the reconciliation of the Cash-in-Bank balances.

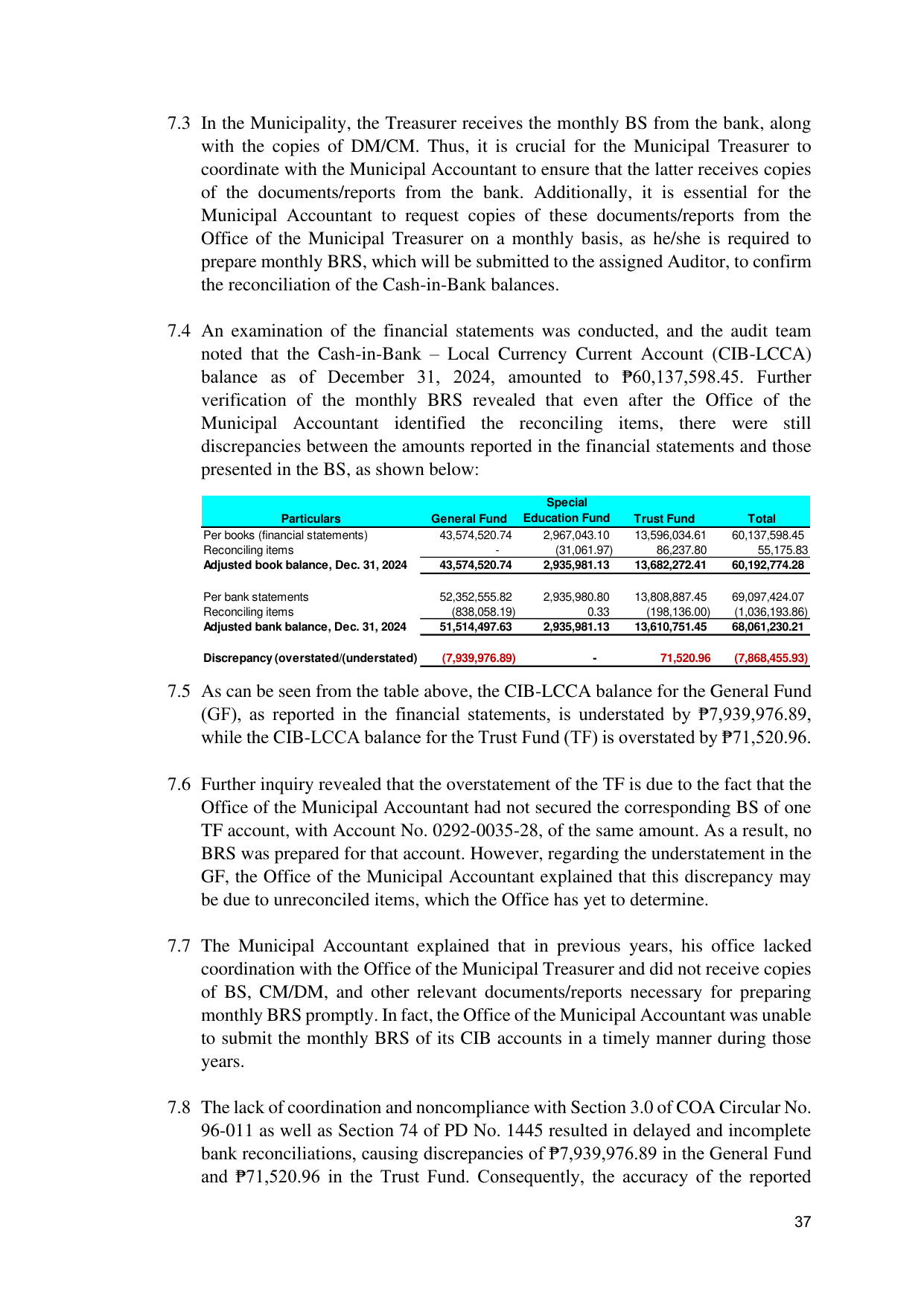

7.4 An examination of the financial statements was conducted, and the audit team

noted that the Cash-in-Bank – Local Currency Current Account (CIB-LCCA)

balance as of December 31, 2024, amounted to ₱60,137,598.45. Further

verification of the monthly BRS revealed that even after the Office of the

Municipal Accountant identified the reconciling items, there were still

discrepancies between the amounts reported in the financial statements and those

presented in the BS, as shown below:

Special

Particulars General Fund Education Fund Trust Fund Total

Per books (financial statements) 43,574,520.74 2,967,043.10 13,596,034.61 60,137,598.45

Reconciling items - (31,061.97) 86,237.80 55,175.83

Adjusted book balance, Dec. 31, 2024 43,574,520.74 2,935,981.13 13,682,272.41 60,192,774.28

Per bank statements 52,352,555.82 2,935,980.80 13,808,887.45 69,097,424.07

Reconciling items (838,058.19) 0.33 (198,136.00) (1,036,193.86)

Adjusted bank balance, Dec. 31, 2024 51,514,497.63 2,935,981.13 13,610,751.45 68,061,230.21

Discrepancy (overstated/(understated) (7,939,976.89) - 71,520.96 (7,868,455.93)

7.5 As can be seen from the table above, the CIB-LCCA balance for the General Fund

(GF), as reported in the financial statements, is understated by ₱7,939,976.89,

while the CIB-LCCA balance for the Trust Fund (TF) is overstated by ₱71,520.96.

7.6 Further inquiry revealed that the overstatement of the TF is due to the fact that the

Office of the Municipal Accountant had not secured the corresponding BS of one

TF account, with Account No. 0292-0035-28, of the same amount. As a result, no

BRS was prepared for that account. However, regarding the understatement in the

GF, the Office of the Municipal Accountant explained that this discrepancy may

be due to unreconciled items, which the Office has yet to determine.

7.7 The Municipal Accountant explained that in previous years, his office lacked

coordination with the Office of the Municipal Treasurer and did not receive copies

of BS, CM/DM, and other relevant documents/reports necessary for preparing

monthly BRS promptly. In fact, the Office of the Municipal Accountant was unable

to submit the monthly BRS of its CIB accounts in a timely manner during those

years.

7.8 The lack of coordination and noncompliance with Section 3.0 of COA Circular No.

96-011 as well as Section 74 of PD No. 1445 resulted in delayed and incomplete

bank reconciliations, causing discrepancies of ₱7,939,976.89 in the General Fund

and ₱71,520.96 in the Trust Fund. Consequently, the accuracy of the reported

37