Account Title Amount

Extraordinary and Miscellaneous Expense ₱ 6,230,515.21

Training Expenses 2,434,615.34

Honoraria 544,500.00

Subsidy to Other Funds 130,000.00

Donations 101,612.50

Salaries and Wages – Casual/ Contractual 98,274.67

Office Equipment 76,793.28

Semi-Expendable Agricultural and Forestry Equipment 47,952.00

Accountable Forms, Plates and Stickers 44,640.00

Repairs and maintenance – Transportation Equipment 37,083.10

Welfare Goods for Distribution 28,000.00

Subscription Expenses 24,200.00

Disaster Response and Rescue Equipment 5,856.00

Office Supplies Inventory 2,839.28

Total ₱ 9,806,881.38

6.4 Apart from the Chart of Accounts recommended by the Commission, Section 51

of the General Provisions, General Appropriations Act (GAA) of CY 2024

provides that Extraordinary and Miscellaneous Expenses (EME) encompass costs

incurred for meetings, seminars and conferences, official entertainment, public

relations, educational, athletic and cultural activities, contributions to civic or

charitable institutions, membership in government associations, membership in

national professional organizations accredited by the Professional Regulation

Commission, membership in the Integrated Bar or the Philippines, subscription to

professional technical journals and informative magazines, library books and

materials, office equipment and supplies, and other similar expenses not supported

by the regular budget allocation.

6.5 However, it is emphasized that the statutory limitation on the disbursements for

EME or discretionary funds shall be observed. We refer Management to Section

325(h) of RA No. 7160, which mandates that the annual appropriations for

discretionary purposes of the local chief executive shall not exceed two percent of

the actual receipts derived from basic real property taxes in the next preceding

calendar year.

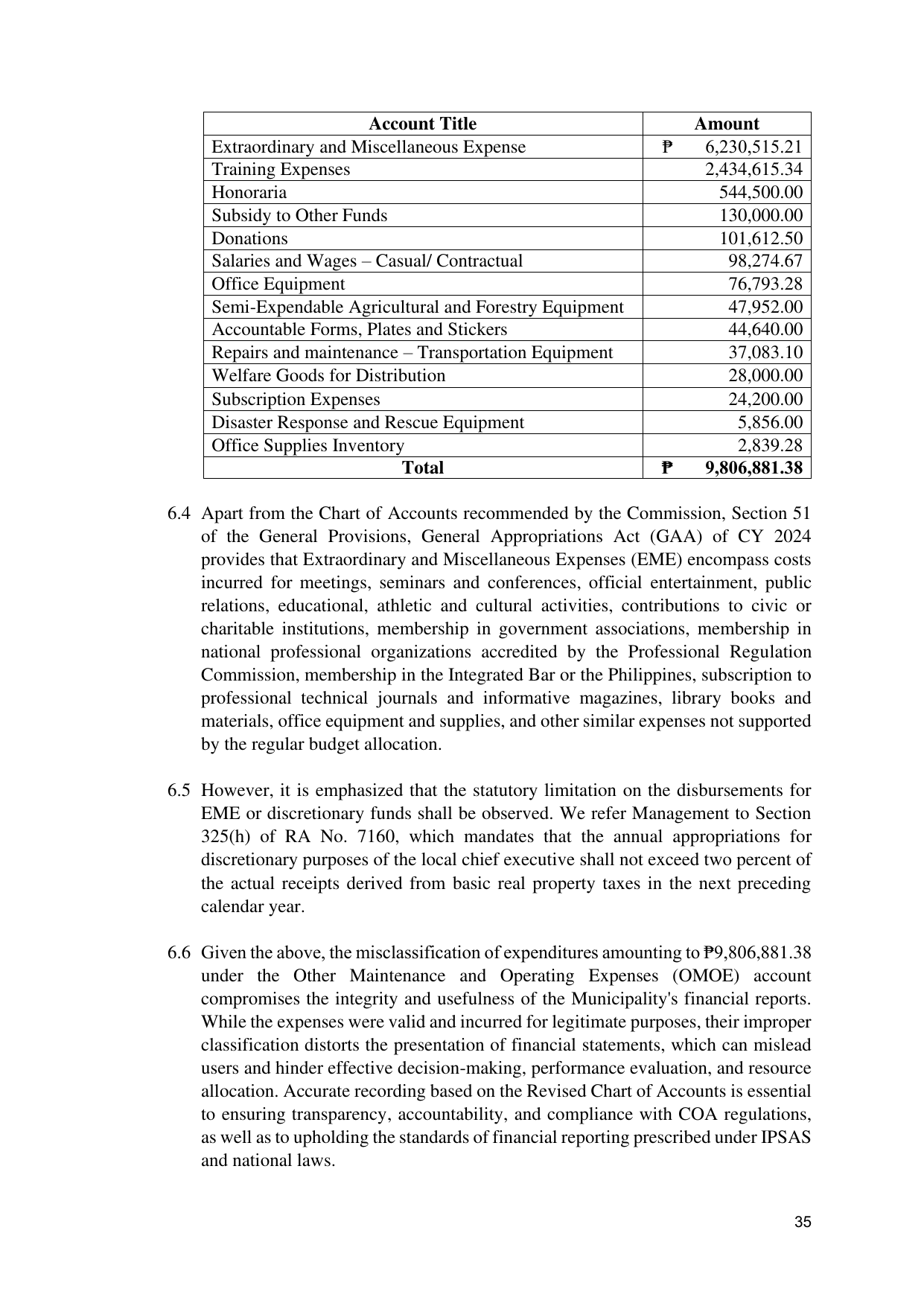

6.6 Given the above, the misclassification of expenditures amounting to ₱9,806,881.38

under the Other Maintenance and Operating Expenses (OMOE) account

compromises the integrity and usefulness of the Municipality's financial reports.

While the expenses were valid and incurred for legitimate purposes, their improper

classification distorts the presentation of financial statements, which can mislead

users and hinder effective decision-making, performance evaluation, and resource

allocation. Accurate recording based on the Revised Chart of Accounts is essential

to ensuring transparency, accountability, and compliance with COA regulations,

as well as to upholding the standards of financial reporting prescribed under IPSAS

and national laws.

35