Page 77 of 113

Ref.

Audit Observations Audit Recommendations Status of Implementation

Circular No. 77-61 dated September 26, Driver’s Trip Tickets to ensure that all the

1977, thus, the reasonableness of fuel data needed to determine the

consumption and the necessity of the trips reasonableness of fuel consumed for the

undertaken could not be determined. period and the necessity of the trips

undertaken are provided.

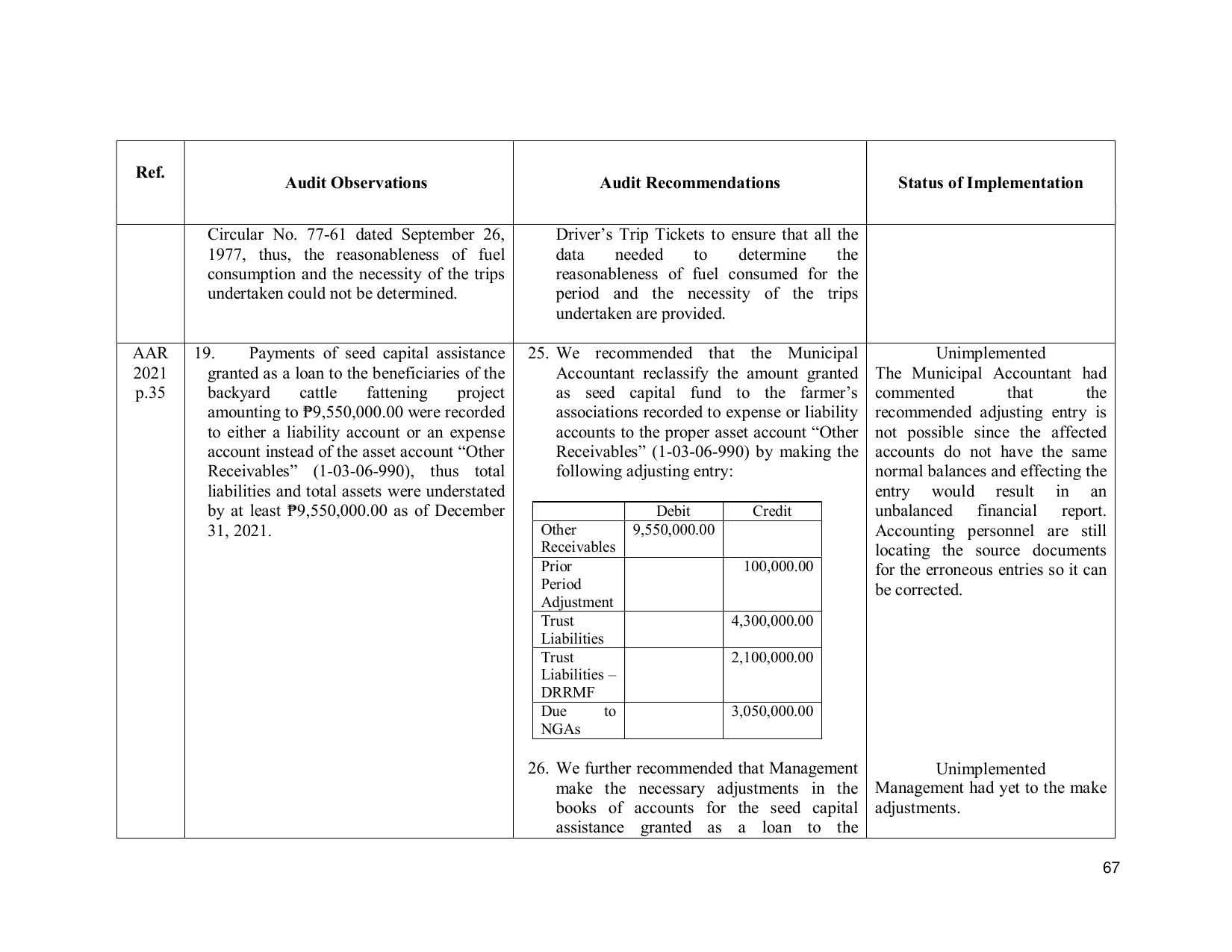

AAR 19. Payments of seed capital assistance 25. We recommended that the Municipal Unimplemented

2021 granted as a loan to the beneficiaries of the Accountant reclassify the amount granted The Municipal Accountant had

p.35 backyard cattle fattening project as seed capital fund to the farmer’s commented that the

amounting to ₱9,550,000.00 were recorded associations recorded to expense or liability recommended adjusting entry is

to either a liability account or an expense accounts to the proper asset account “Other not possible since the affected

account instead of the asset account “Other Receivables” (1-03-06-990) by making the accounts do not have the same

Receivables” (1-03-06-990), thus total following adjusting entry: normal balances and effecting the

liabilities and total assets were understated entry would result in an

by at least ₱9,550,000.00 as of December Debit Credit unbalanced financial report.

31, 2021. Other 9,550,000.00 Accounting personnel are still

Receivables locating the source documents

Prior 100,000.00 for the erroneous entries so it can

Period be corrected.

Adjustment

Trust 4,300,000.00

Liabilities

Trust 2,100,000.00

Liabilities –

DRRMF

Due to 3,050,000.00

NGAs

26. We further recommended that Management Unimplemented

make the necessary adjustments in the Management had yet to the make

books of accounts for the seed capital adjustments.

assistance granted as a loan to the

67