Delinquent RPT and SET

8. Delinquent Real Property Taxes (RPT) and Special Education Taxes (SET)

including penalties accruing thereon which accumulated to ₱23,751,277.85

remained uncollected as of December 31, 2024, depriving the Municipality of

substantial amount of income which could have been utilized to finance the

implementation of various development projects or other major

programs/projects/activities (PPAs).

8.1. Section 254 of Republic Act (RA) 7160 provides that:

“(a) When the real property tax or any other tax imposed under this Title

becomes delinquent, the xxx municipal treasurer shall immediately cause

a notice of the delinquency to be posted at the main entrance of the xxx

municipal hall and in a publicly accessible and conspicuous place in

each barangay of the local government unit concerned. The notice of

delinquency shall also be published once a week for two (2) consecutive

weeks, in a newspaper of general circulation in the xxx municipality.

(b) Such notice shall specify the date upon which the tax became

delinquent and shall state that personal property may be distrained to

effect payment. It shall likewise state that at any time before the

distraint of personal property, payment of the tax with surcharges,

interests and penalties may be made xxx, and unless the tax, surcharges

and penalties are paid before the expiration of the year for which the

tax is due except when the notice of assessment or special levy is

contested administratively or judicially pursuant to the provisions of

Chapter 3, Title II, Book II of this Code, the delinquent real property

will be sold at public auction, and the title to the property will be vested

in the purchaser, subject, however, to the right of the delinquent owner

of the property or any person having legal interest therein to redeem

the property within one (1) year from the date of sale.”

8.2. Furthermore, Section 270 of the same Act provides that the collection of basic RPT

and any other tax levied should be made within five (5) years from the date they

become due and that no action for the collection of the tax, whether administrative

or judicial, shall be instituted after the expiration of such period.

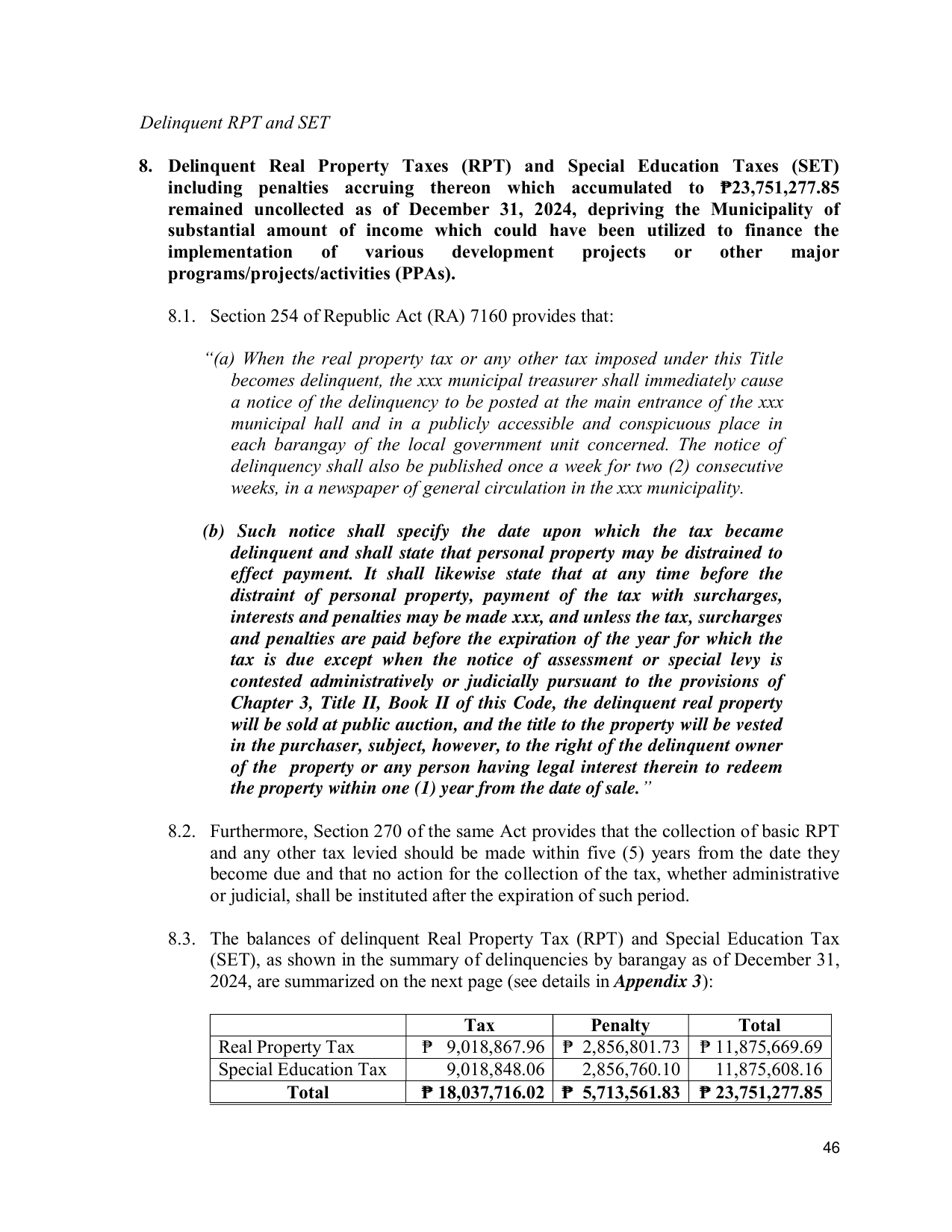

8.3. The balances of delinquent Real Property Tax (RPT) and Special Education Tax

(SET), as shown in the summary of delinquencies by barangay as of December 31,

2024, are summarized on the next page (see details in Appendix 3):

Tax Penalty Total

Real Property Tax ₱ 9,018,867.96 ₱ 2,856,801.73 ₱ 11,875,669.69

Special Education Tax 9,018,848.06 2,856,760.10 11,875,608.16

Total ₱ 18,037,716.02 ₱ 5,713,561.83 ₱ 23,751,277.85

46