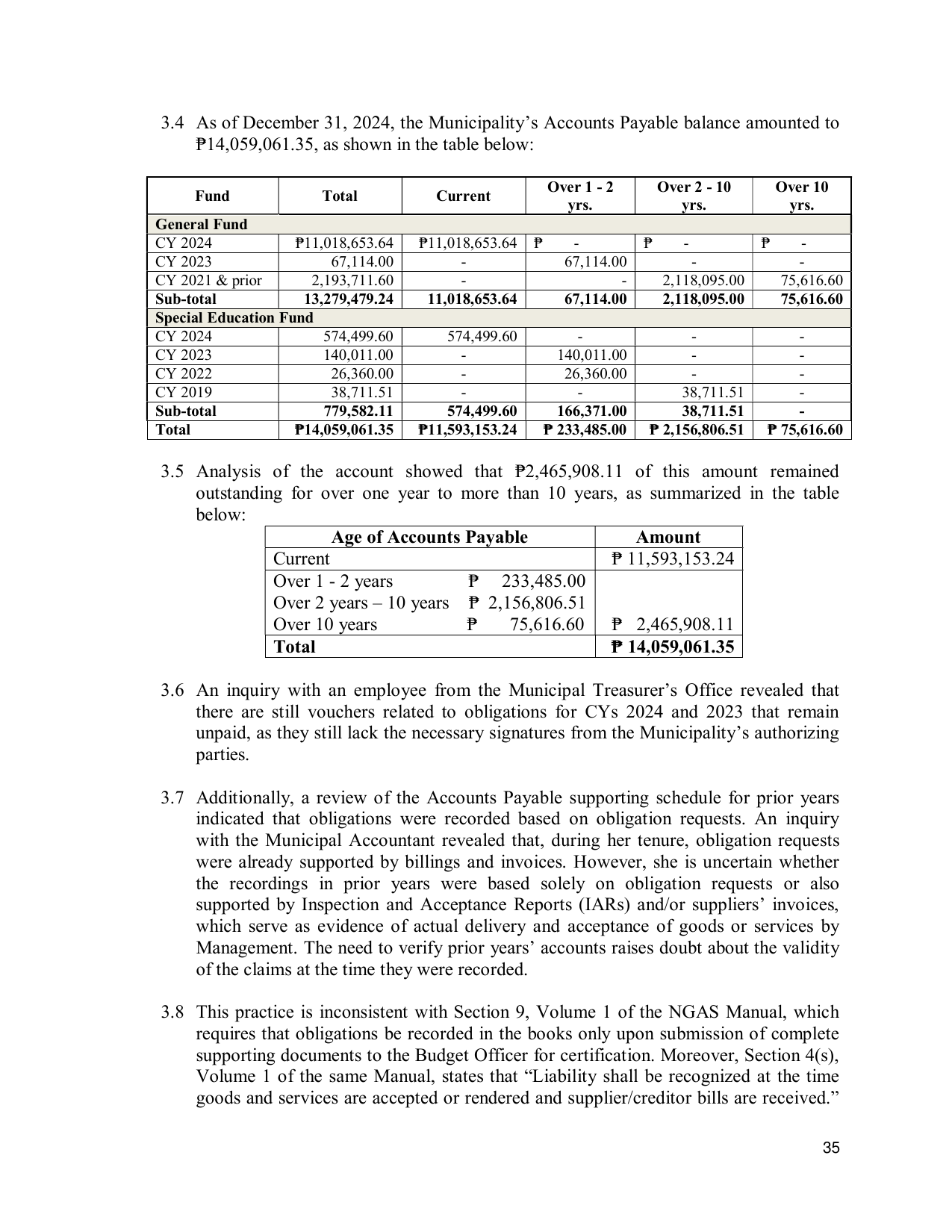

3.4 As of December 31, 2024, the Municipality’s Accounts Payable balance amounted to

₱14,059,061.35, as shown in the table below:

Over 1 - 2 Over 2 - 10 Over 10

Fund Total Current

yrs. yrs. yrs.

General Fund

CY 2024 ₱11,018,653.64 ₱11,018,653.64 ₱ - ₱ - ₱ -

CY 2023 67,114.00 - 67,114.00 - -

CY 2021 & prior 2,193,711.60 - - 2,118,095.00 75,616.60

Sub-total 13,279,479.24 11,018,653.64 67,114.00 2,118,095.00 75,616.60

Special Education Fund

CY 2024 574,499.60 574,499.60 - - -

CY 2023 140,011.00 - 140,011.00 - -

CY 2022 26,360.00 - 26,360.00 - -

CY 2019 38,711.51 - - 38,711.51 -

Sub-total 779,582.11 574,499.60 166,371.00 38,711.51 -

Total ₱14,059,061.35 ₱11,593,153.24 ₱ 233,485.00 ₱ 2,156,806.51 ₱ 75,616.60

3.5 Analysis of the account showed that ₱2,465,908.11 of this amount remained

outstanding for over one year to more than 10 years, as summarized in the table

below:

Age of Accounts Payable Amount

Current ₱ 11,593,153.24

Over 1 - 2 years ₱ 233,485.00

Over 2 years – 10 years ₱ 2,156,806.51

Over 10 years ₱ 75,616.60 ₱ 2,465,908.11

Total ₱ 14,059,061.35

3.6 An inquiry with an employee from the Municipal Treasurer’s Office revealed that

there are still vouchers related to obligations for CYs 2024 and 2023 that remain

unpaid, as they still lack the necessary signatures from the Municipality’s authorizing

parties.

3.7 Additionally, a review of the Accounts Payable supporting schedule for prior years

indicated that obligations were recorded based on obligation requests. An inquiry

with the Municipal Accountant revealed that, during her tenure, obligation requests

were already supported by billings and invoices. However, she is uncertain whether

the recordings in prior years were based solely on obligation requests or also

supported by Inspection and Acceptance Reports (IARs) and/or suppliers’ invoices,

which serve as evidence of actual delivery and acceptance of goods or services by

Management. The need to verify prior years’ accounts raises doubt about the validity

of the claims at the time they were recorded.

3.8 This practice is inconsistent with Section 9, Volume 1 of the NGAS Manual, which

requires that obligations be recorded in the books only upon submission of complete

supporting documents to the Budget Officer for certification. Moreover, Section 4(s),

Volume 1 of the same Manual, states that “Liability shall be recognized at the time

goods and services are accepted or rendered and supplier/creditor bills are received.”

35