Recording of SET in General Fund Books

2. Entries for the Special Education Tax (SET) totaling ₱9,589,520.80 were recorded

in the General Fund’s books instead of the Special Education Fund’s books, which

is inconsistent with Section 235 of RA No. 7160 and Section 88 of the NGAS Manual

for LGUs, Volume I, thus affecting the fair presentation of the SET Receivable and

Deferred SET Income accounts in the financial statements at year-end.

2.1. Section 235 of Republic Act (RA) No. 7160 provides that the proceeds from the

additional levy of one percent (1%) on the assessed value of real property, which

shall be in addition to the basic real property tax, shall exclusively accrue to the

Special Education Fund (SEF).

2.2. Section 88 of the New Government Accounting System (NGAS) Manual for Local

Government Units (LGUs), Volume I, also specifies that in accounting for the SEF,

the Chief Accountant must maintain separate registries for appropriation, allotment,

and obligations as well as books of accounts for the SEF.

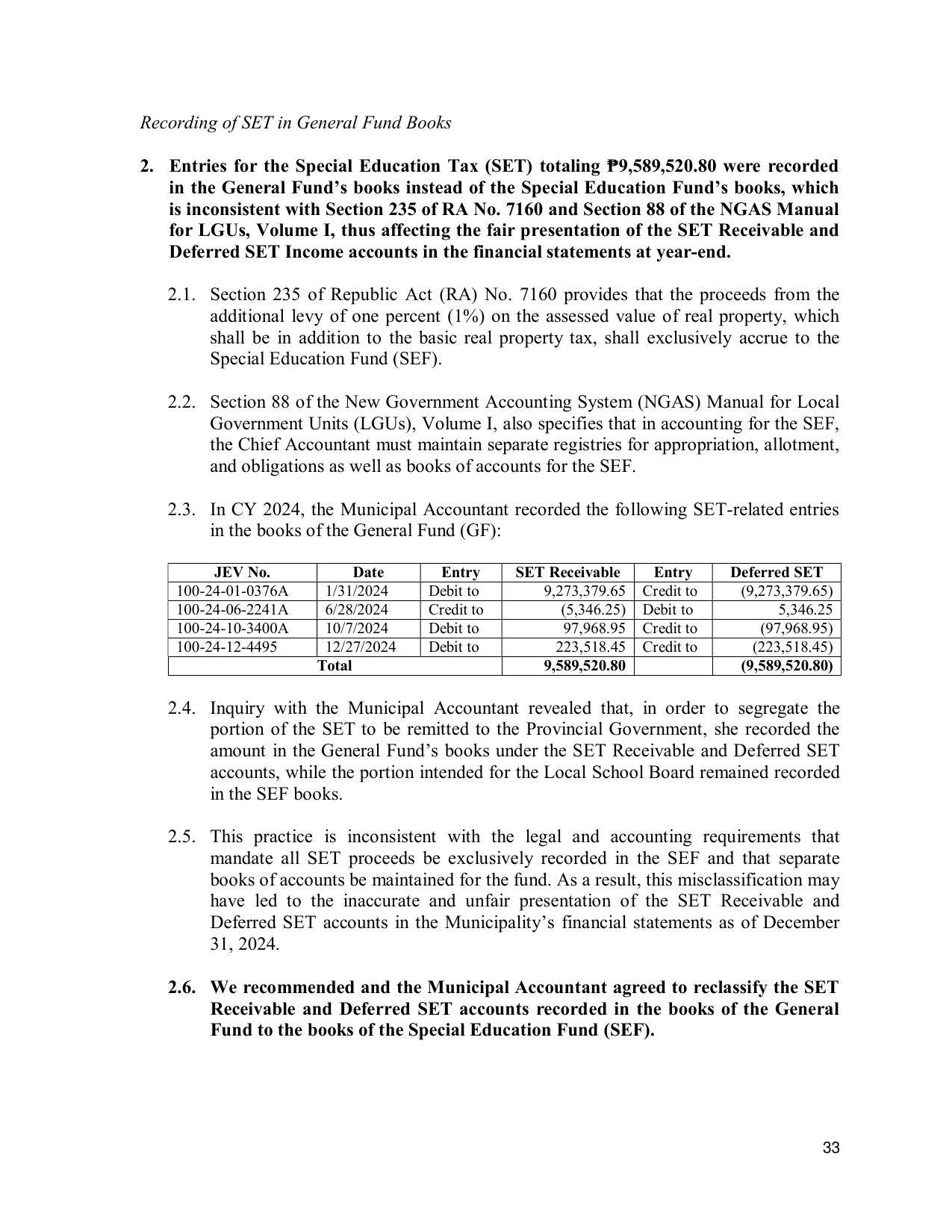

2.3. In CY 2024, the Municipal Accountant recorded the following SET-related entries

in the books of the General Fund (GF):

JEV No. Date Entry SET Receivable Entry Deferred SET

100-24-01-0376A 1/31/2024 Debit to 9,273,379.65 Credit to (9,273,379.65)

100-24-06-2241A 6/28/2024 Credit to (5,346.25) Debit to 5,346.25

100-24-10-3400A 10/7/2024 Debit to 97,968.95 Credit to (97,968.95)

100-24-12-4495 12/27/2024 Debit to 223,518.45 Credit to (223,518.45)

Total 9,589,520.80 (9,589,520.80)

2.4. Inquiry with the Municipal Accountant revealed that, in order to segregate the

portion of the SET to be remitted to the Provincial Government, she recorded the

amount in the General Fund’s books under the SET Receivable and Deferred SET

accounts, while the portion intended for the Local School Board remained recorded

in the SEF books.

2.5. This practice is inconsistent with the legal and accounting requirements that

mandate all SET proceeds be exclusively recorded in the SEF and that separate

books of accounts be maintained for the fund. As a result, this misclassification may

have led to the inaccurate and unfair presentation of the SET Receivable and

Deferred SET accounts in the Municipality’s financial statements as of December

31, 2024.

2.6. We recommended and the Municipal Accountant agreed to reclassify the SET

Receivable and Deferred SET accounts recorded in the books of the General

Fund to the books of the Special Education Fund (SEF).

33