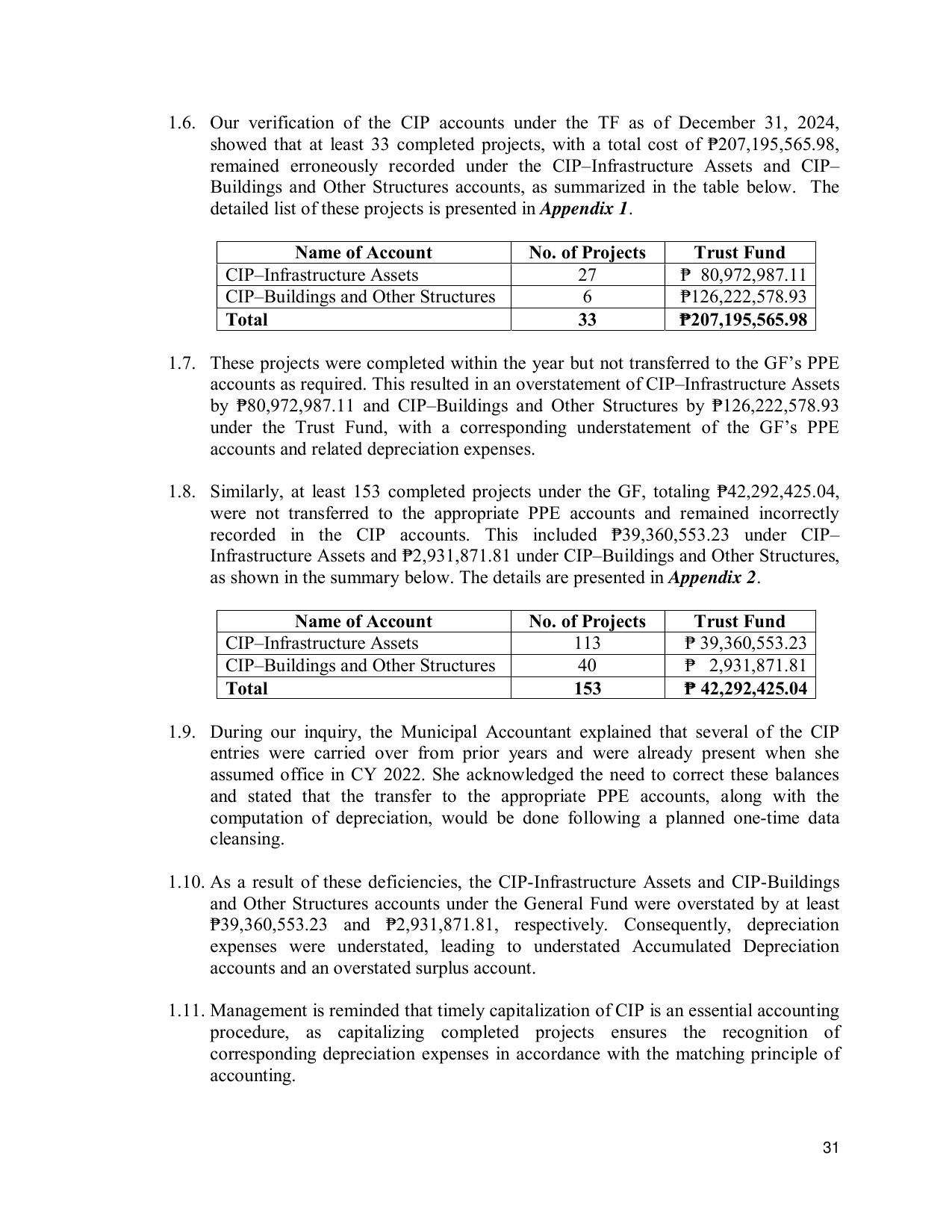

1.6. Our verification of the CIP accounts under the TF as of December 31, 2024,

showed that at least 33 completed projects, with a total cost of ₱207,195,565.98,

remained erroneously recorded under the CIP–Infrastructure Assets and CIP–

Buildings and Other Structures accounts, as summarized in the table below. The

detailed list of these projects is presented in Appendix 1.

Name of Account No. of Projects Trust Fund

CIP–Infrastructure Assets 27 ₱ 80,972,987.11

CIP–Buildings and Other Structures 6 ₱126,222,578.93

Total 33 ₱207,195,565.98

1.7. These projects were completed within the year but not transferred to the GF’s PPE

accounts as required. This resulted in an overstatement of CIP–Infrastructure Assets

by ₱80,972,987.11 and CIP–Buildings and Other Structures by ₱126,222,578.93

under the Trust Fund, with a corresponding understatement of the GF’s PPE

accounts and related depreciation expenses.

1.8. Similarly, at least 153 completed projects under the GF, totaling ₱42,292,425.04,

were not transferred to the appropriate PPE accounts and remained incorrectly

recorded in the CIP accounts. This included ₱39,360,553.23 under CIP–

Infrastructure Assets and ₱2,931,871.81 under CIP–Buildings and Other Structures,

as shown in the summary below. The details are presented in Appendix 2.

Name of Account No. of Projects Trust Fund

CIP–Infrastructure Assets 113 ₱ 39,360,553.23

CIP–Buildings and Other Structures 40 ₱ 2,931,871.81

Total 153 ₱ 42,292,425.04

1.9. During our inquiry, the Municipal Accountant explained that several of the CIP

entries were carried over from prior years and were already present when she

assumed office in CY 2022. She acknowledged the need to correct these balances

and stated that the transfer to the appropriate PPE accounts, along with the

computation of depreciation, would be done following a planned one-time data

cleansing.

1.10. As a result of these deficiencies, the CIP-Infrastructure Assets and CIP-Buildings

and Other Structures accounts under the General Fund were overstated by at least

₱39,360,553.23 and ₱2,931,871.81, respectively. Consequently, depreciation

expenses were understated, leading to understated Accumulated Depreciation

accounts and an overstated surplus account.

1.11. Management is reminded that timely capitalization of CIP is an essential accounting

procedure, as capitalizing completed projects ensures the recognition of

corresponding depreciation expenses in accordance with the matching principle of

accounting.

31