Page 37 of 113

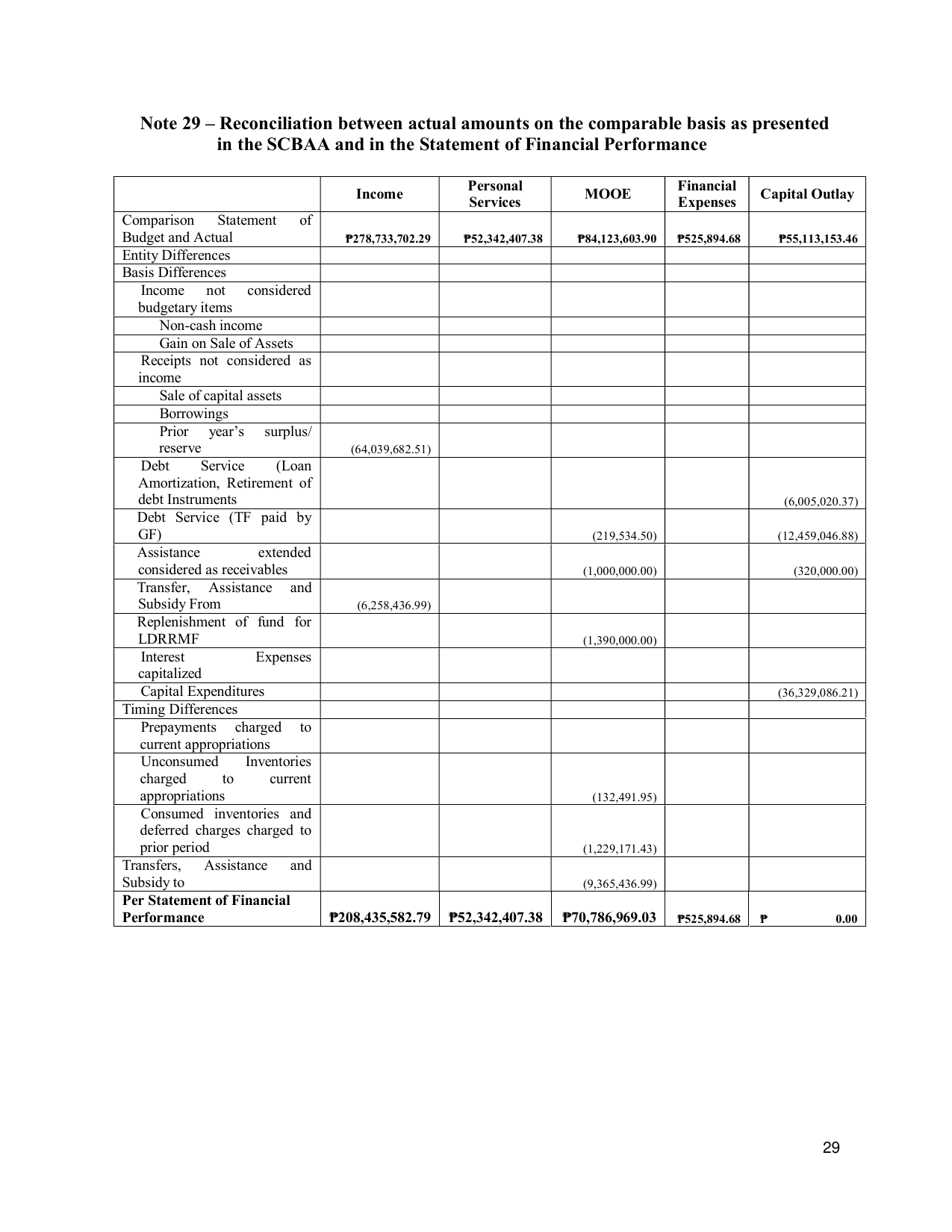

Note 29 – Reconciliation between actual amounts on the comparable basis as presented

in the SCBAA and in the Statement of Financial Performance

Personal Financial

Income MOOE Capital Outlay

Services Expenses

Comparison Statement of

Budget and Actual ₱278,733,702.29 ₱52,342,407.38 ₱84,123,603.90 ₱525,894.68 ₱55,113,153.46

Entity Differences

Basis Differences

Income not considered

budgetary items

Non-cash income

Gain on Sale of Assets

Receipts not considered as

income

Sale of capital assets

Borrowings

Prior year’s surplus/

reserve (64,039,682.51)

Debt Service (Loan

Amortization, Retirement of

debt Instruments (6,005,020.37)

Debt Service (TF paid by

GF) (219,534.50) (12,459,046.88)

Assistance extended

considered as receivables (1,000,000.00) (320,000.00)

Transfer, Assistance and

Subsidy From (6,258,436.99)

Replenishment of fund for

LDRRMF (1,390,000.00)

Interest Expenses

capitalized

Capital Expenditures (36,329,086.21)

Timing Differences

Prepayments charged to

current appropriations

Unconsumed Inventories

charged to current

appropriations (132,491.95)

Consumed inventories and

deferred charges charged to

prior period (1,229,171.43)

Transfers, Assistance and

Subsidy to (9,365,436.99)

Per Statement of Financial

Performance ₱208,435,582.79 ₱52,342,407.38 ₱70,786,969.03 ₱525,894.68 ₱ 0.00

29