3.10 Financial liabilities

The LGU’s financial liabilities include payables and borrowings which the

Municipality is committed to pay for goods or services received. It also

includes amounts entrusted/withheld from outside sources/offices and

personnel for which the Municipality is acting as a trustee or administrator.

Payables are recognized and recorded in the books of accounts only upon

acceptance of goods and rendition of services to the Municipality.

Loans contracted by the Municipality are recognized upon receipt of the

proceeds from creditors.

3.11 Equity

Equity represents the difference between assets and liabilities. The amount

available for operations is computed by deducting the following from the

ending balance of Government Equity:

a. equity set aside to finance capital projects with appropriations provided in

the previous years (continuing appropriations)

b. portion pertaining to receivables, inventories, prepayments and other

current assets

c. portion pertaining to property, plant and equipment including public

infrastructures in process

d. amount reserved for Local Disaster Risk Reduction and Management

Fund

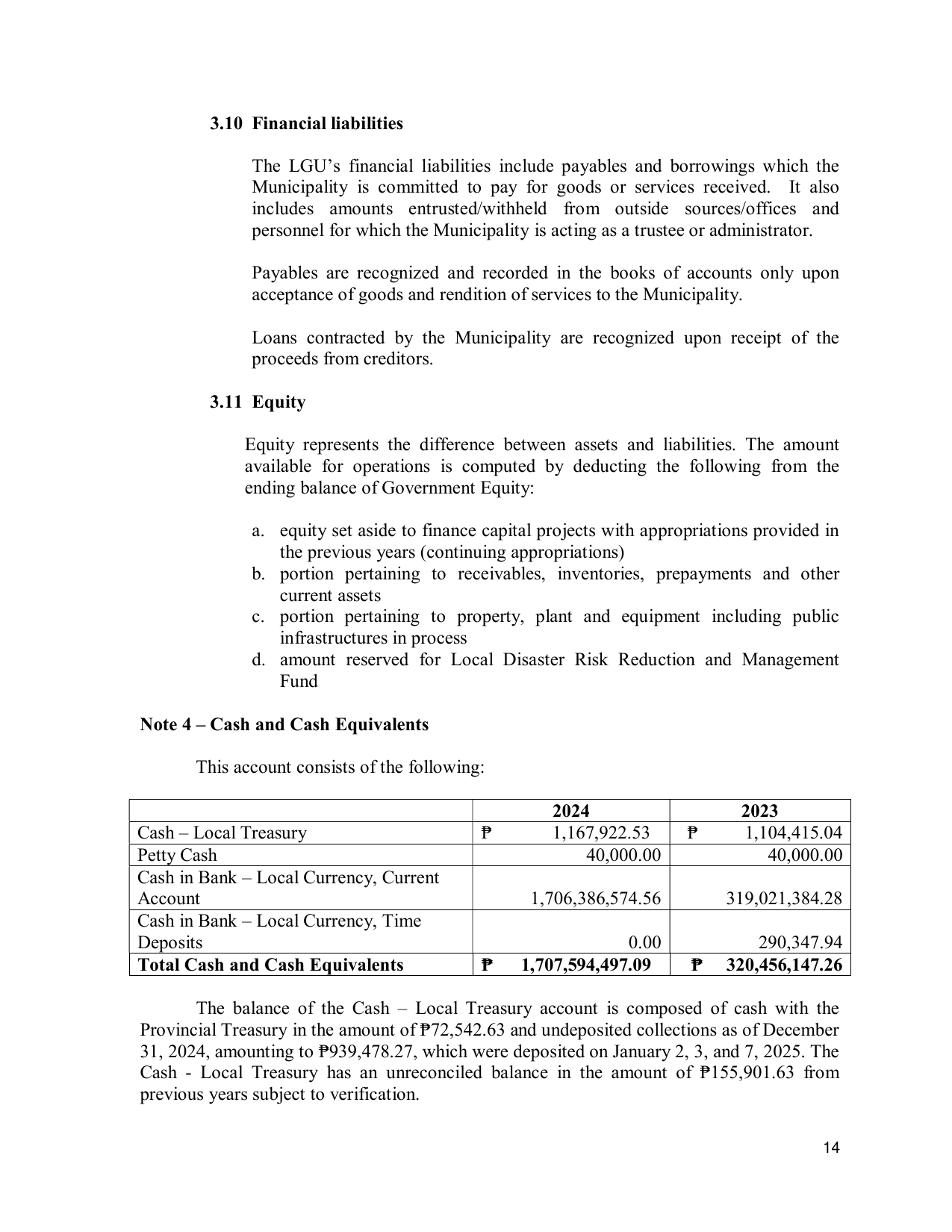

Note 4 – Cash and Cash Equivalents

This account consists of the following:

2024 2023

Cash – Local Treasury ₱ 1,167,922.53 ₱ 1,104,415.04

Petty Cash 40,000.00 40,000.00

Cash in Bank – Local Currency, Current

Account 1,706,386,574.56 319,021,384.28

Cash in Bank – Local Currency, Time

Deposits 0.00 290,347.94

Total Cash and Cash Equivalents ₱ 1,707,594,497.09 ₱ 320,456,147.26

The balance of the Cash – Local Treasury account is composed of cash with the

Provincial Treasury in the amount of ₱72,542.63 and undeposited collections as of December

31, 2024, amounting to ₱939,478.27, which were deposited on January 2, 3, and 7, 2025. The

Cash - Local Treasury has an unreconciled balance in the amount of ₱155,901.63 from

previous years subject to verification.

14