prolonged inaction or write-off of dormant receivables that could otherwise be

recovered.

51. We recommended and the Municipal Accountant agreed to ensure the timely

preparation and submission of the Semestral Report on the Status of Unliquidated

Cash Advances, Fund Transfers, and Other Receivables on or before the 8th day

following the end of each semester, in compliance with Section 122 of P.D. 1445

and COA Memorandum 2017-010 dated May 15, 2017.

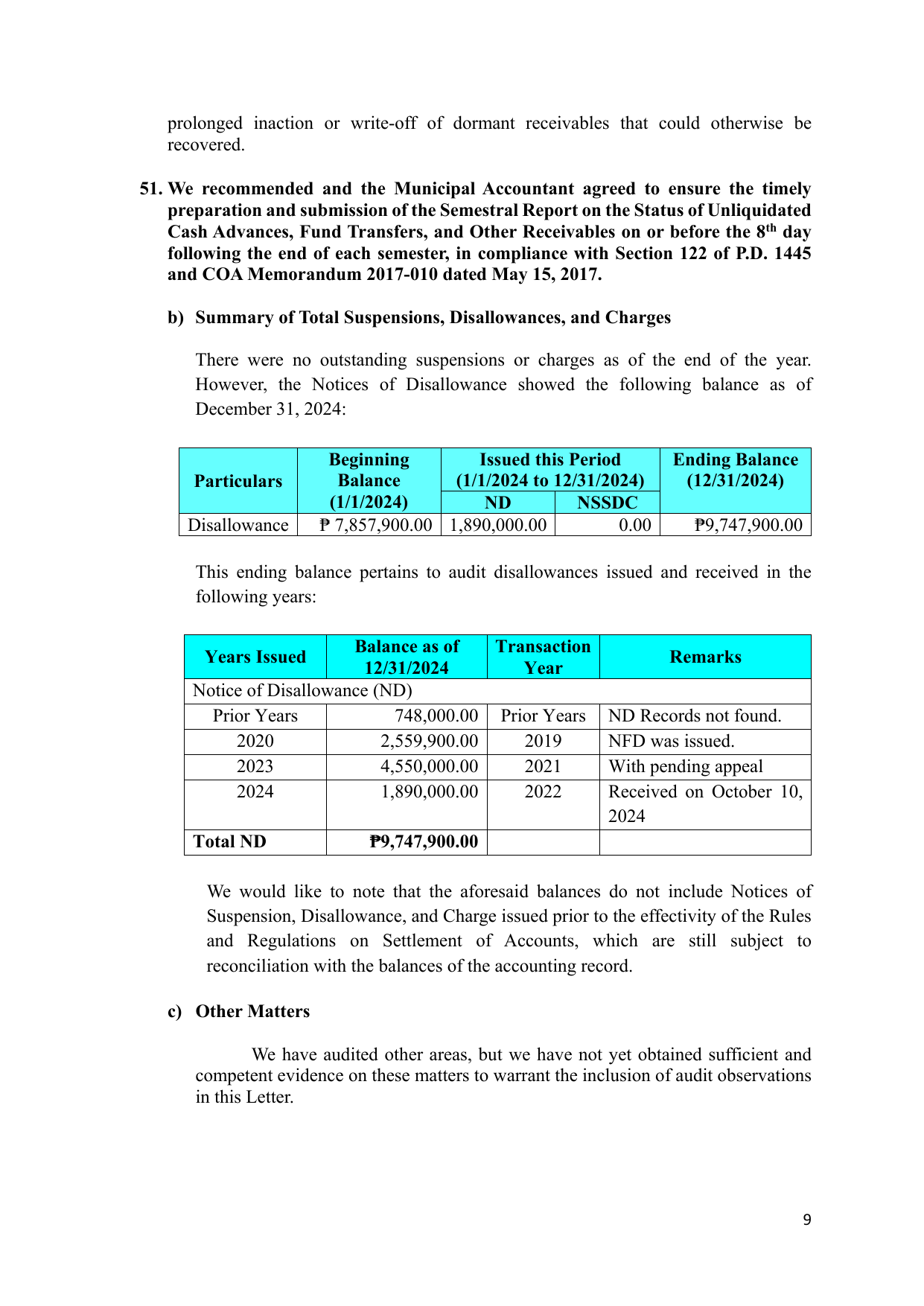

b) Summary of Total Suspensions, Disallowances, and Charges

There were no outstanding suspensions or charges as of the end of the year.

However, the Notices of Disallowance showed the following balance as of

December 31, 2024:

Beginning Issued this Period Ending Balance

Particulars Balance (1/1/2024 to 12/31/2024) (12/31/2024)

(1/1/2024) ND NSSDC

Disallowance ₱ 7,857,900.00 1,890,000.00 0.00 ₱9,747,900.00

This ending balance pertains to audit disallowances issued and received in the

following years:

Balance as of Transaction

Years Issued Remarks

12/31/2024 Year

Notice of Disallowance (ND)

Prior Years 748,000.00 Prior Years ND Records not found.

2020 2,559,900.00 2019 NFD was issued.

2023 4,550,000.00 2021 With pending appeal

2024 1,890,000.00 2022 Received on October 10,

2024

Total ND ₱9,747,900.00

We would like to note that the aforesaid balances do not include Notices of

Suspension, Disallowance, and Charge issued prior to the effectivity of the Rules

and Regulations on Settlement of Accounts, which are still subject to

reconciliation with the balances of the accounting record.

c) Other Matters

We have audited other areas, but we have not yet obtained sufficient and

competent evidence on these matters to warrant the inclusion of audit observations

in this Letter.

9